/Monolithic%20Power%20System%20Inc%20logo%20and%20stock%20chart-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

With a market cap of $32.2 billion, Monolithic Power Systems, Inc. (MPWR) is a leading semiconductor company specializing in high-performance, integrated power solutions. The Kirkland, Washington-based company designs, develops, and markets energy-efficient power management chips used across a wide range of industries, including automotive, industrial, cloud computing, consumer electronics, and telecommunications.

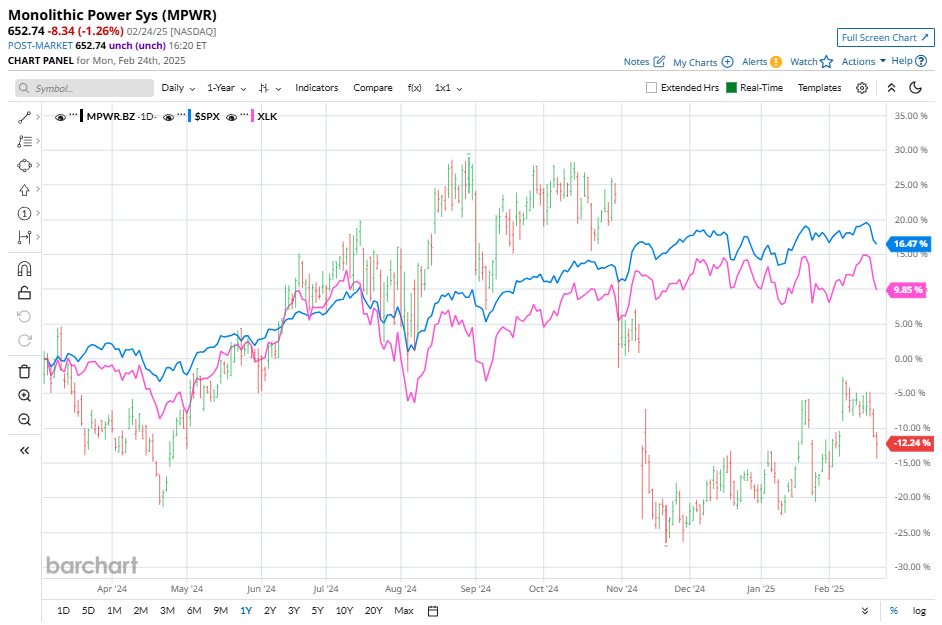

Shares of the chips company have underperformed the broader market over the past 52 weeks. MPWR stock has dropped 9.5% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 17.6%. But 2025 tells a different story. MPWR is staging a comeback, surging 10.3% year-to-date and leaving the S&P 500’s modest 1.7% gain in the dust.

Looking closer, it has also lagged behind the Technology Select Sector SPDR Fund's (XLK) 12.8% return over the past 52 weeks. However, it has outpaced XLK’s marginal YTD fall.

On Feb. 6, Monolithic Power posted its Q4 earnings, and its shares popped 9% in the next trading session. Its revenue of $621.7 million, up 36.9% year over year, with non-GAAP EPS rising 42% to $4.09, driven by strong performance in the Automotive and Enterprise Data segments. Looking forward, Management’s Q1 revenue guidance of $610–$630 million surpassed the $578.1 million consensus estimate.

For the current fiscal year, ending in December, analysts expect MPWR's EPS to grow 23.6% year-over-year to $13.20. The company's earnings surprise history is mixed. It beat the consensus estimates in two of the last four quarters while missing on two other occasions.

Among the 13 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on eight “Strong Buy” ratings, two “Moderate Buys,” and three “Holds.”

This consensus has been fairly consistent over the past months.

On Feb. 7, Loop Capital raised Monolithic Power’s price target to $760 from $660 while maintaining a “Buy” rating. The firm highlighted MPWR’s Q4 results and Q1 guidance, noting its continued market share gains in the PMIC and analog sectors. Strong data center revenue and broader cyclical strength further support the company’s better-than-seasonal Q1 outlook.

MPWR’s mean price target of $840.58 represents a 28.8% premium to the prevailing market prices. The Street-high price target of $1,100 implies a potential upside of 68.5%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.