TheStreet aims to feature only the best products and services. If you buy something via one of our links, we may earn a commission.

Car insurance is required to drive legally in almost every state. Liability insurance is a must, but full coverage — which is optional and includes comprehensive and collision insurance — could be worth the added cost if you drive a newer vehicle.

Having the right level of coverage is crucial to avoid having to pay out of pocket after an accident. Experts often recommend at least 100/300/100 in liability coverage, but each person’s insurance needs are different. To make an informed decision about how much coverage to purchase, let’s start by understanding the various components of auto insurance and how they work together.

What is car insurance?

Drivers purchase car insurance to protect themselves and their assets in the event of an accident. Policies can cover three types of losses:

- Injuries or property damage that you cause to others. Liability insurance pays for injuries or damage you inflict upon another person or their property. Almost all states require drivers to carry a minimum amount of liability insurance, but that amount varies from state to state and may be insufficient to cover the costs associated with a major accident.

- Damage to your own vehicle. Collision and comprehensive coverage — typically bundled with liability insurance as full-coverage car insurance — will pay for physical damage to your own vehicle. Collision insurance covers accidents where your vehicle strikes another car or a stationary object. Comprehensive covers your car from theft, vandalism, severe weather and other non-collision events. States do not require such insurance, but if you have a vehicle that is financed or leased, your lender may require it.

- Injuries to yourself or to your passengers. Some forms of car insurance can pay for your medical expenses. States with no-fault insurance laws — which require you to file a claim with your own insurer, regardless of who was at fault — typically require personal injury protection (PIP) coverage to pay for these costs. In other states, you may be able to purchase medical payments (MedPay) insurance to cover such expenses.

Shutterstock

What types of car insurance are there?

As you shop for car insurance, you are likely to see a variety of coverage options. Some types of insurance are mandatory while others are not.

Liability coverage

With few exceptions, states require drivers to carry a minimal amount of liability insurance. However, carrying a low level of liability coverage could result in you paying a significant amount of money out of pocket after an accident.

State requirements vary, but a typical state minimum-liability insurance policy may offer only 25/50/25 in coverage. That breaks down to:

- $25,000 for bodily injury, per person

- $50,000 in bodily injury, per accident

- $25,000 in property damage per incident

Experts recommend getting as much liability insurance as you can afford, at minimum 50/100/50. But some insurance agents recommend more.

“I don’t think anyone should have less than $300,000 in liability,” says Karl Susman, industry expert and owner of Susman Insurance Agency in Los Angeles. As for physical coverage, he notes: “It’s not hard to get $100,000 damage on a car nowadays.”

Others in the field encourage drivers to consider even higher limits. Michael Silverman of Silver Lining Insurance Agency in New York recommends his clients carry $500,000 combined single-limit insurance along with an umbrella policy for additional liability coverage.

States may also mandate other types of coverage such as underinsured/uninsured motorist coverage. If you live in a state with no-fault insurance laws, you will also need to have personal injury protection (PIP) coverage.

Related: 10 major ways to maximize your savings on a big car expense now

Collision and comprehensive coverage

Collision insurance covers damage to your vehicle that is a result of colliding with another vehicle or striking a stationary object like a building.

Comprehensive insurance applies to non-collision damage to your vehicle caused by things like fires or storms, as well as vandalism and theft.

Typically bundled together as part of full-coverage car insurance, comprehensive and collision will cover your vehicle up to its current fair market value or actual cash value (ACV), minus any deductible you may have. Both kinds of coverage are optional, unless you are financing or leasing a car. In that case, your lender or leasing company may require it.

But even if you paid cash for your car, this kind of insurance could be worth the added cost.

If you don’t have enough savings or liquid assets to repair or replace your car after a serious accident, then buying collision and comprehensive coverage is often advisable. If you are looking for a way to make this insurance more affordable, consider changing your deductible.

“The higher the deductible, the lower the premium,” Silverman says.

More on car insurance

- Cheapest car insurance companies in 2024

- Will my insurance go up if I move?

- What is the penalty for driving without insurance in your state?

Personal injury protection (PIP)

In states with no-fault insurance laws, you must file a claim with your own personal injury protection (PIP) insurance if you are injured in an accident — you can’t file a claim with the other party’s carrier, even if they are at fault.

Like liability minimums, state-mandated PIP levels can be quite low. For instance, the PIP requirement in Florida is only $10,000.

You may be able to purchase more than the minimum though. For instance, Michigan has a $250,000 minimum for non-Medicaid-covered drivers, but residents can purchase PIP with $500,000 and unlimited coverage as well.

Medical payments coverage (MedPay)

Maine is one of the only states to require drivers to purchase medical payments (MedPay) coverage, but it is offered as optional coverage in many other states.

“It will literally just pay for medical bills,” Susman says. For instance, if your child’s friend closes their hand in your car door, it will cover any medical bills associated with the incident. Given their low coverage limits, this isn’t insurance to be used after a major accident.

While Susman says he doesn’t see MedPay on policies as often as he did in the past, its cost is negligible so people may want to consider it.

Uninsured/underinsured motorist coverage

Uninsured (UM) and underinsured (UIM) insurance protects you if you’re in an accident where the at-fault driver either does not have car insurance or has insufficient coverage. It also applies if you’re struck by a hit-and-run driver.

UI/UIM insurance has two parts:

- UM/UIM liability insurance covers medical bills for yourself and your passengers, as well as lost wages, funeral/burial/cremation costs, as well as pain and suffering.

- UI/UIM property damage insurance applies to physical damage that your vehicle sustains as a result of being struck by an uninsured or underinsured motorist.

This coverage is mandatory in some states and optional in others.

More from TheStreet on car insurance

- Car insurance companies quietly use these apps to hike your rates

- 10 major ways to maximize your savings on car insurance

- Auto insurance companies have found a sneaky way to increase prices

Other optional coverages

Outside these main insurance types, your car insurance company may also offer the following:

Windshield glass. Repairs to cracked or damaged windshields are typically covered by comprehensive policies, but in some states you may be able to buy separate windshield glass coverage at a nominal cost.

Roadside assistance. This optional coverage pays for towing costs or similar expenses should you find yourself stranded with an inoperable vehicle. Before signing up for this coverage, make sure you don’t already have roadside coverage through another source such as a credit card or car warranty.

Rental car reimbursement. If your car is damaged in an accident, your insurance company will cover the cost of a rental while it’s being repaired if you have this coverage.

Gap insurance. In the event your car is totaled, gap insurance will cover the difference between what the car is worth and how much you still owe if it was leased or financed. Gap insurance may be offered by lenders and car dealers as well as insurance companies.

Getty Images

How much car insurance do I need?

When it comes to determining the right level of coverage to purchase, you should consider the following:

- Your state’s requirements (e.g., liability insurance, personal injury protection (PIP), uninsured/underinsured motorist).

- Your financial assets, including cash on hand, to cover any damages as if you were not insured.

- Other existing insurance you have that may cover auto-related claims, such as umbrella liability policies.

Case study: How does car insurance work?

So, let’s consider how this all can play out in real life.

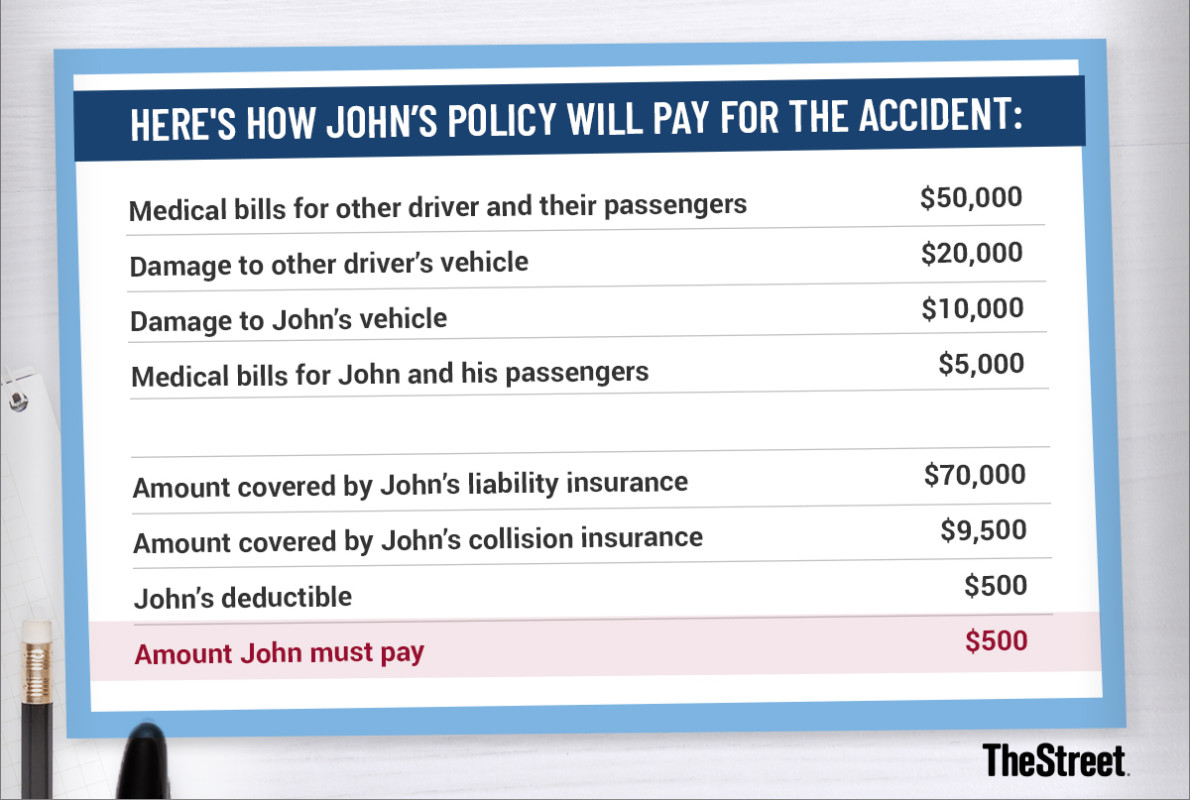

In our case study, John has opted to purchase full coverage with liability limits of 100/300/100. In the event of an at-fault accident, this will pay $100,000 for bodily injuries per person and up to $300,000 per incident. Plus, it covers up to $100,000 in property damage. His collision and comprehensive coverage has a $500 deductible.

One day, John fails to yield at a stop sign and hits another car. The other driver and their passengers are injured, and their medical bills total $50,000. The damage to their car is appraised at $20,000. John’s car has $15,000 in damage, and he and his passengers have $5,000 in medical costs.

The following graphic offers some details on how John's policy will pay for the accident:

TheStreet

How are car insurance rates determined?

Car insurance companies set rates based on how likely they think you are to file a claim and how much that claim will cost them. Some of the factors they consider include:

Driver demographics. Younger, inexperienced drivers will pay higher insurance rates than older, experienced drivers, according to the National Association of Insurance Commissioners (NAIC). In addition, males pay more than similarly aged females, and single people pay more than married couples, according to NAIC data.

Location. Insurers also base their rates in part on the ZIP code where the vehicle is kept. Those in urban centers typically pay more than drivers in suburban or rural communities, in part due to the increased density and associated higher risk rates.

Driving record. If you have even a single speeding ticket, your rates are likely to increase at renewal time. The same goes if you’ve been in an at-fault accident or convicted of a DUI or DWI. Insurers will raise rates if someone has an unsafe record and, therefore, a higher chance of filing a claim.

Credit history. In all but a handful of states, your credit history can be used to determine rates. Limiting the amount of debt you carry and making payments on time can help boost your credit overall and lead to future savings.

Type of coverage. The more coverage you require, the more it will cost. A state-minimum liability policy will be far cheaper than full-coverage insurance, but the bare minimum also leaves you far more vulnerable financially if you’re in a major accident.

Type of vehicle. An insurance company will also consider how much it will cost to repair or replace your vehicle if it is in an accident or stolen. Luxury vehicles may cost more to insure while more modest vehicles could have lower premiums.

Discounts. Carriers tout a variety of savings for everything from bundling policies to pay-per-mile insurance. While some discounts are applied automatically, it is a good idea to check in with your agent or insurer each year to see if there are any you may be missing.

Shutterstock

Frequently asked questions

What is a deductible?

A deductible is the amount of money you must pay out of pocket before your insurer will pay for collision and comprehensive claims. For example, if it will cost $2,000 to repair your car and you have a $500 deductible, your insurer will pay $1,500.

Policies with low deductibles (such as $200 or less) will cost more than those with deductibles of $500 or $1,000. Before raising your deductible to save money on insurance, though, be sure you have enough in savings to cover the new deductible should you have to file a claim.

How much liability insurance do I need?

By law, you need coverage that meets your state’s minimum liability limits. Your insurer should be able to provide this information, or you can contact your state’s insurance department.

If you are leasing or financing your car, you may be required to purchase insurance with higher levels – 100/300/50 is the standard for leasing companies, Silverman says.

Talk to an insurance agent or other trusted advisor to determine how much liability insurance is advisable given your financial situation.

How much car insurance do I need in California?

Motor vehicle liability policies in California must meet the following minimum requirements:

- $15,000 for injury/death to one person.

- $30,000 for injury/death to more than one person.

- $5,000 for damage to property.

Related: Veteran fund manager sees world of pain coming for stocks

TheStreet aims to feature only the best products and services. If you buy something via one of our links, we may earn a commission. The products featured here have been independently reviewed. This article has been edited and published by TheStreet. Learn more.