Asana (NYSE:ASAN) is preparing to release its quarterly earnings on Thursday, 2024-12-05. Here's a brief overview of what investors should keep in mind before the announcement.

Analysts expect Asana to report an earnings per share (EPS) of $-0.07.

Investors in Asana are eagerly awaiting the company's announcement, hoping for news of surpassing estimates and positive guidance for the next quarter.

It's worth noting for new investors that stock prices can be heavily influenced by future projections rather than just past performance.

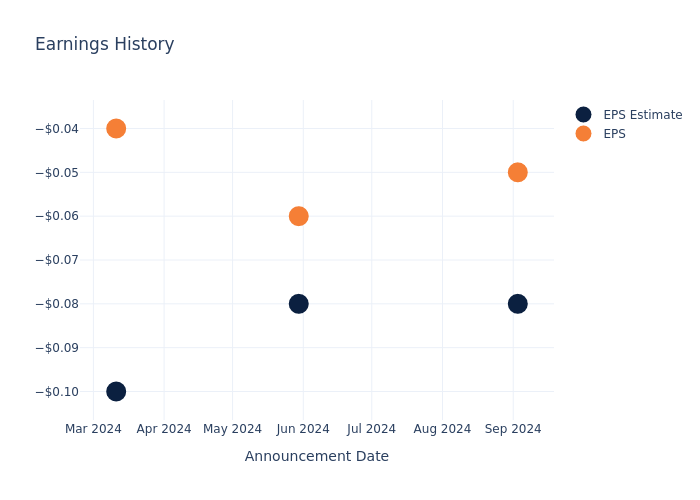

Historical Earnings Performance

During the last quarter, the company reported an EPS beat by $0.03, leading to a 5.12% drop in the share price on the subsequent day.

Analysts' Take on Asana

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on Asana.

The consensus rating for Asana is Neutral, derived from 3 analyst ratings. An average one-year price target of $12.67 implies a potential 16.53% downside.

Analyzing Ratings Among Peers

In this analysis, we delve into the analyst ratings and average 1-year price targets of DoubleVerify Hldgs, AvePoint and Agilysys, three key industry players, offering insights into their relative performance expectations and market positioning.

- The prevailing sentiment among analysts is an Buy trajectory for DoubleVerify Hldgs, with an average 1-year price target of $23.84, implying a potential 57.05% upside.

- Analysts currently favor an Neutral trajectory for AvePoint, with an average 1-year price target of $15.0, suggesting a potential 1.19% downside.

- The consensus among analysts is an Buy trajectory for Agilysys, with an average 1-year price target of $135.12, indicating a potential 790.12% upside.

Peer Analysis Summary

The peer analysis summary outlines pivotal metrics for DoubleVerify Hldgs, AvePoint and Agilysys, demonstrating their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Asana | Neutral | 10.31% | $159.22M | -23.60% |

| DoubleVerify Hldgs | Buy | 17.77% | $140.08M | 1.63% |

| AvePoint | Neutral | 22.05% | $67.58M | 1.23% |

| Agilysys | Buy | 16.49% | $43.21M | 0.53% |

Key Takeaway:

Asana ranks at the bottom for Revenue Growth among its peers. It is also at the bottom for Gross Profit. However, Asana is at the top for Return on Equity.

Discovering Asana: A Closer Look

Asana is a provider of collaborative work management software delivered via a cloud-based SaaS model. The firm's solution offers scalable, dynamic tools to improve the efficiency of project and process management across countless use cases, including marketing programs, managing IT approvals, and performance management. Asana's offering supports workflow management across teams, provides real time visibility into projects, and reporting and automation capabilities. The firm generates revenue via software subscriptions on a per seat basis.

Asana: Delving into Financials

Market Capitalization Analysis: With a profound presence, the company's market capitalization is above industry averages. This reflects substantial size and strong market recognition.

Positive Revenue Trend: Examining Asana's financials over 3 months reveals a positive narrative. The company achieved a noteworthy revenue growth rate of 10.31% as of 31 July, 2024, showcasing a substantial increase in top-line earnings. As compared to its peers, the revenue growth lags behind its industry peers. The company achieved a growth rate lower than the average among peers in Information Technology sector.

Net Margin: Asana's net margin surpasses industry standards, highlighting the company's exceptional financial performance. With an impressive -40.28% net margin, the company effectively manages costs and achieves strong profitability.

Return on Equity (ROE): Asana's ROE is below industry standards, pointing towards difficulties in efficiently utilizing equity capital. With an ROE of -23.6%, the company may encounter challenges in delivering satisfactory returns for shareholders.

Return on Assets (ROA): The company's ROA is below industry benchmarks, signaling potential difficulties in efficiently utilizing assets. With an ROA of -7.51%, the company may need to address challenges in generating satisfactory returns from its assets.

Debt Management: Asana's debt-to-equity ratio stands notably higher than the industry average, reaching 0.94. This indicates a heavier reliance on borrowed funds, raising concerns about financial leverage.

To track all earnings releases for Asana visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.