/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

Nvidia (NVDA) will release its fourth quarter financials for its fiscal 2025 on Wednesday, Feb. 26. NVDA stock has seen some turbulence since its last earnings report as its Q4 revenue guidance fell short of Wall Street’s expectations.

Moreover, the market is also wary of shrinking margins and questions surrounding the long-term sustainability of artificial intelligence (AI) spending. Notably, Nvidia has been at the center of the AI boom, but a new challenger emerged in late January with the launch of DeepSeek’s R1 model. The Chinese startup’s claim that it could build a large language model (LLM) at a fraction of the expected cost rattled the market, with Nvidia taking a significant hit. If companies can develop advanced AI with significantly less computing power, demand for Nvidia’s high-powered GPUs could face headwinds.

While Nvidia stock has remained under pressure, it is still up about 74% over the past year. The stock’s notable growth reflects AI-driven demand for its GPUs.

Heading into the print, the market will be looking for reassurance from management that AI infrastructure spending will sustain and potentially expand, even as technological advancements make AI development more efficient. This could trigger a rally in Nvidia shares. However, any signs of weakness could further pressure NVDA stock. With that backdrop, let's explore the expectations for Q4.

Nvidia: Q4 Expectations

Nvidia is gearing up for another blockbuster quarter, with management projecting Q4 revenue of $37.5 billion, plus or minus 2%. The midpoint of this forecast reflects year-over-year growth of about 70%. The solid demand for its Hopper architecture and the initial ramp-up of its next-gen Blackwell products will likely support its top line. While supply constraints remain a challenge, Nvidia is on track to exceed its previous Blackwell revenue estimates of several billion dollars as supply expands.

Notably, Nvidia has been on a remarkable growth streak, consistently outpacing expectations with strong revenue and earnings. The company’s growth is largely driven by the widespread adoption of accelerated computing and AI across industries.

One of the key catalysts has been its data center business, which continues to hit record-breaking revenue. The segment witnessed unprecedented demand for its Hopper platform, with sales of the H200 chip soaring into the double-digit billions, marking the fastest product ramp in Nvidia’s history.

Beyond data centers, Nvidia’s AI PC segment is gaining momentum, while its automotive business is benefiting from growing demand for self-driving technologies. These tailwinds are expected to provide further upside for the company’s top-line growth.

While Nvidia’s revenue could continue to climb, its profit margins could face some short-term pressure as it scales up Blackwell. The platform offers a customizable AI infrastructure with multiple Nvidia chips, diverse networking options, and configurations for both air- and liquid-cooled data centers. Currently, the company focuses on meeting overwhelming demand and expanding availability, which could temporarily impact margins.

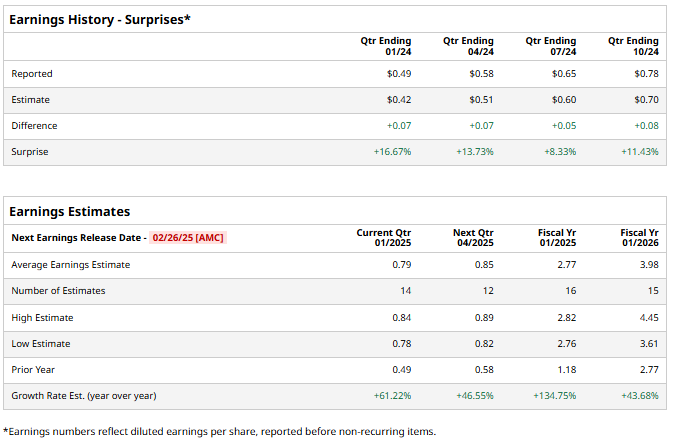

Despite this, Wall Street remains optimistic. Analysts expect Nvidia to deliver earnings per share (EPS) of $0.79, reflecting an impressive 61.2% year-over-year increase.

Overall, Nvidia is poised to deliver another strong quarter, with solid top- and bottom-line growth. However, the trajectory of NVDA stock will depend on the broader AI investment landscape. The market will closely monitor management’s commentary on AI spending trends and demand outlook, as these factors will shape the company’s next growth phase.

The Road Ahead for Nvidia Stock

As Nvidia announces its Q4 results, the broader AI investment landscape will play a significant role in determining the stock’s trajectory. The market will look for clear signals that AI infrastructure spending remains strong, and that demand for Nvidia’s GPUs will continue to expand.

Meanwhile, Wall Street analysts remain highly optimistic, with Nvidia holding a “Strong Buy” consensus rating. The average price target of $176.95 suggests upside potential of nearly 32% from current levels. Analysts’ bullish outlook suggests that they expect the spending on AI infrastructure will likely sustain. Moreover, the solid demand for NVDA’s Hopper and Blackwell platforms suggests that the company is well-positioned for continued growth. Moreover, Nvidia’s expanding customer base and diversified revenue streams strengthen its long-term growth outlook.