Searching for RMD Tables Online?

If you do an online search for the new RMD (Required Minimum Distribution) tables to use to calculate your 2022 RMD, you might find yourself running in circles. Where, just where, are those 2022 tables? The online searches I tried today take you to the old tables, even if you specifically search for 2022 RMD tables.

So, be careful. Don’t assume the tables you are finding online are for 2022.

Official RMD Tables for 2022 RMDs

The official place to look for the tables that apply for 2022 RMDs is the 2021 IRS Pub. 590-B, called “Distributions from Individual Retirement Arrangements (IRAs).”

If you hunt hard enough, you can find the draft version of IRS Pub. 590-B for 2021, which was released on Jan. 5. It is located in the IRS’s section on draft tax forms. The regulations that adopted the new tables are found at regulations.gov.

The current IRS Pub. 590-B on IRS.gov is for use in preparing 2020 (not 2021) returns. It does not have the new tables to be used for 2022 RMDs.

Most IRA owners will need the Uniform Table (Table III in Pub. 590-B). Another table applies to IRA owners whose spouse is more than 10 years younger and yet another for those who inherit IRAs. Be sure to confirm which table applies to you, and always check with your tax adviser before taking any RMD actions.

The Uniform Table For Use in 2022

So, here it is.

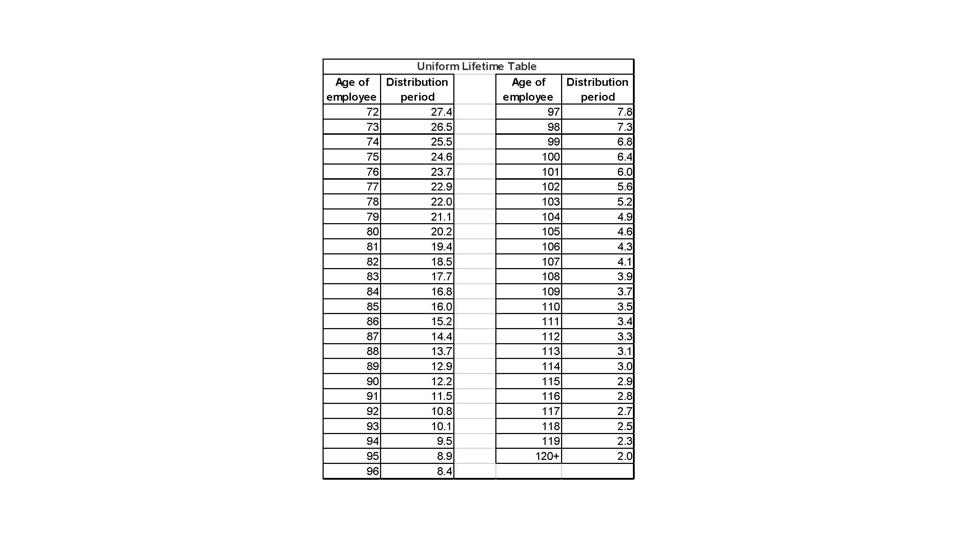

Uniform Lifetime Table (to calculate 2022 RMDs for IRA Owners)

For use by unmarried owners; married owners whose spouses aren’t more than 10 years younger; married owners whose spouses aren’t the sole beneficiaries of their IRAs.

Doing the Calculation

The Uniform Lifetime Table (also called Table III) shows the “distribution period” — that’s the divisor you use to calculate your RMD based on your 12/31/2021 balance.

To show you how to use the table, let’s do a simple example together. Assume you have a tax-deferred IRA with a balance of $500,000 at 12/31/2021. You are age 74. Your sole beneficiary is your wife, who is 72 years old. To calculate your RMD, look up the distribution period for age 74, which is 25.5. Divide $500,000 by 25.5 to get your 2022 RMD of $19,608.

That’s the RMD amount that you will need to take out of your IRA before 12/31/2022 using the new 2022 tables. The figure is slightly less than the RMD calculated under the old tables in effect in 2021. The RMD under the old tables would be $21,008 based on the age of 74 and a divisor of 23.8 (assuming a 12/31/2020 value of $500,000).

IRS Publication 590-B for 2021 Is Coming Soon

While you can’t find the 2021 IRS Pub. 590-B for use in filing your 2021 returns just yet (that’s the one you want to see for 2022 RMDs), it won’t be long. It’s in the works and coming soon. In the meantime, be careful calculating RMDs based on tables you might find online that have not yet been updated. But, also note that since the new tables require a slightly smaller RMD, you won’t be too far off if you do use the earlier tables.

Questions?

To keep up with topics that I cover, be sure to follow me on the forbes.com site (and if you would like to subscribe, check out the red box at the top right). Write to me at forbes@juliejason.com. Include your city and state, and mention that you are a forbes.com reader. While all questions cannot be answered, each email is read and reviewed and can lead to discussion in a future post.