DKosig for iStockphoto; Canva

What Caused the Financial Crisis of 2007–2008? How Did it Start?

Mortgages sold to U.S. homeowners were responsible for a series of events that caused trillions of dollars in investment losses around the world, nearly collapsing the global financial system and resulting in the Great Recession, the worst economic downturn since the Great Depression.

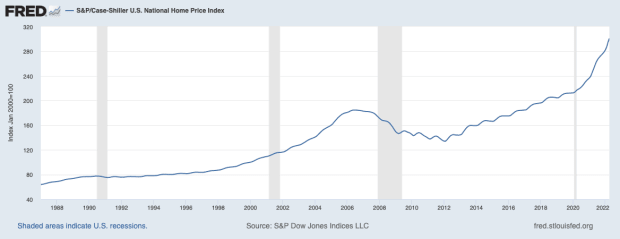

It all began with the U.S. housing market, which in the 1990s and early 2000s was the place to be. Red-hot demand had caused home prices to increase by more than 100 percent in less than 10 years. Housing-related industries made up almost half of all new jobs created, and construction starts had more than doubled.

S&P Dow Jones Indices LLC, S&P/Case-Shiller U.S. National Home Price Index [CSUSHPINSA], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/CSUSHPINSA, July 5, 2022.

Expanded credit and low sustained interest rates by the Federal Reserve created the perfect environment for new homebuyers. But unfortunately, a lack of oversight at both ends of the financial spectrum would result in massive defaults.

On the consumer end, predatory lenders had targeted low-income individuals with the prospect of owning their own home through a newly introduced mortgage category: a subprime mortgage. These loans were made to borrowers with less-than-perfect credit scores, often requiring no proof of income or even a down payment. They featured adjustable rates which started low but then would “reset” to a higher rate every year—or whenever prevailing interest rates increased.

Subprime mortgages were poorly explained and complex in nature. Borrowers did not understand what they were getting into, and when the Fed began a series of interest rate hikes to curb inflation between 2004 and 2006, millions could not pay their substantially more expensive mortgages and ended up defaulting. Banks were left to cover the losses, but they had an even bigger problem on their hands.

How Did Banks Contribute to the Financial Crisis?

Banks simply make their profits by selling loans and gaining interest on their loans. They can also make money via loan securitization, in which groups of loans are pooled together into interest-bearing packages known as mortgage-backed securities (MBS).

One type of MBS, known as collateralized mortgage obligations (CMOs), was further subdivided into slices, or tranches, containing thousands of subprime mortgages. Each tranche had its own distinct credit rating and yield. The AAA-rated categories were the highest rated and considered the least likely to default because borrowers were deemed capable of meeting their financial commitments. Packaged loans rated BBB or lower were riskier and more likely to default; yet, they also offered the highest yields.

CMOs were sold to investment banks, which saw this type of security as another investment vehicle and traded them around the world for profits. In fact, the main buyers of CMOs were institutional investors, like hedge funds, pension funds, money market funds, and insurance companies. These groups comprised what was known as the shadow banking industry, which received little regulatory oversight. Some investment banks packaged AAA-rated securities with lower-quality ones, and these bundles were passed off as top-rated securities when they were sold to investors.

All continued apace until an asset bubble formed in housing, with speculation driving prices ever skyward. The bubble peaked in early 2006 and then quickly bottomed out.

What Happened When the Housing Bubble Burst?

A number of things happened when the housing bubble made its spectacular burst:

- The Federal Reserve had raised the Fed Funds Rate 17 times from 1.0% to 5.25%. Homeowners suddenly found themselves with mortgages that cost more than their homes were worth, and housing demand fell.

- At the same time, interest rates on subprime mortgages adjusted higher, and millions of homeowners were unable to repay and went into default.

- Because millions of housing loans could not be repaid, subprime mortgage lenders went into bankruptcy. New Century Financial Corp., one of the biggest issuers of subprime mortgages, was the first to fall, and dozens more followed.

- When the housing bubble burst, the assets that backed them became worthless; the bond funding for CMOs also collapsed. Investment banks and the shadow banking industry could not raise funds from securities markets. A panic broke out, causing a selloff of “toxic debt” around the world. Banks experienced a credit crunch, which meant they no longer had the funds to lend to one another, sending many to the brink of insolvency. Bundled securities passed off with top ratings collapsed as the value of lower-rated securities dropped.

- On September 15, 2008, Lehman Brothers, one of the world’s largest investment banks and heavily leveraged in subprime debt, declared bankruptcy—the largest in U.S. history. The federal government had to step in with emergency capital to avoid a global financial meltdown, subsequently bailing out other companies, such as the insurance company AIG, and arranging for Bank of America to purchase investment banker Merrill Lynch for $50 billion in stock. It also provided emergency capital to keep Bear Stearns, another investment bank engaged in packaging MBS, afloat.

- In response to the collapse of Lehman Brothers, the Dow Jones Industrial Average fell more than 500 points at one point in September 2008, for its largest single-day point decline in almost a decade. Fearing bank runs, investors pulled $196 billion from money market accounts. The economy nose-dived into an 18-month tailspin known as the Great Recession.

How Did Fannie Mae and Freddie Mac Contribute to the Financial Crisis?

Government-sponsored enterprises, like Fannie Mae and Freddie Mac, had a mandate to make home ownership affordable by providing liquidity to banks and mortgage providers, which could, in turn, originate even more mortgages.

Fannie Mae and Freddie Mac had used leverage to take on more than $5 trillion loan guarantees during this period and suffered incredible losses as a result of the subprime crisis. In fact, had the federal government not stepped in to bail them out, they would have become insolvent.

On September 6, 2008, the Federal Housing Finance Agency put Fannie Mae and Freddie Mac under conservatorship and provided them with $190 billion in emergency funding. Because they were no longer shareholder governed, they were delisted from the New York Stock Exchange.

Fannie Mae was also to blame for its role in bundling and selling CMOs—specifically because they were guaranteed by the U.S. government. Credit-rating agencies, like Standard & Poor’s, Moody’s, and Fitch, erroneously gave these bundles of subprime mortgages AAA ratings when they were, in fact, far riskier.

As a result, 76 percent of subprime-filled CMOs were downgraded to junk status by 2010, resulting in writedowns or losses amounting to more than half a trillion dollars.

Contagion Effect Leading to Global Financial Crisis

The financial markets’ collapse in the U.S. had a contagion effect that spread to other countries, with many economists dubbing it a global financial crisis. The U.S. is often regarded as a safe investment destination, and when stock and bond prices there dropped precipitously in late 2008, nations with strong economic and financial ties to the U.S. suffered and saw their markets decline in sympathy. Many nations used the U.S. dollar as the primary source for their international reserves but afterward sought to diversify their reserves with other currencies.

How Was the Financial Crisis of 2007–2008 Resolved?

In September 2008, Congress approved the “Bailout Bill,” which provided $700 billion to add emergency liquidity to the markets. Through the Troubled Asset Relief Program (TARP) passed in October 2008, the U.S. Treasury added billions more to stabilize financial markets—including buying equity in banks. Also, through TARP, investment banks like Goldman Sachs and Morgan Stanley changed their charters and transitioned into commercial banks.

Between 2008 and 2014, the Federal Reserve slashed interest rates to nearly 0 percent.

It also began a series of quantitative easing measures which added more than $4 trillion to the financial system and thus encouraged banks to loan again—to each other as well as to consumers.

Many homeowners, struggling to avoid home foreclosure, received housing credits, and in 2011 President Barack Obama approved a program that would allow borrowers to refinance their loans even though they were “underwater,” or that the value of their homes was less than the amount that had to repay of their remaining mortgage.

In order to reform the financial industry and prevent future financial crises, in 2010, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act. Dodd-Frank limited future speculative trading by banks. In addition, it created the Consumer Financial Protection Bureau to safeguard consumers against further predatory lending practices.

In addition, credit-rating agencies received more stringent oversight and now must display greater transparency. For instance, they are now authorized to issue ratings on structured products, like CMOs, only so long as they have obtained and published information about their underlying assets.

Is Another Financial Crisis Coming?

TheStreet.com’s Luc Olinga believes the current crisis in cryptocurrencies has shades of Lehman Brothers written all over it.