Key takeaways

- Claiming the standard deduction is easier, because you don’t have to keep track of expenses. The 2023 standard deduction is $13,850 for single taxpayers ($20,800 if you’re filing as head of household), $27,700 for married taxpayers, and slightly more if you’re over 65.

- If you own a home and the total of your mortgage interest, points, mortgage insurance premiums, and real estate taxes are greater than the standard deduction, you might benefit from itemizing.

- If your state and local taxes—including real estate, property, income, and sales taxes—plus your mortgage interest exceed the standard deduction, you might want to itemize.

- If you paid more than 7.5% of your adjusted gross income for out-of-pocket medical expenses, you might be able to deduct the amount above 7.5%.

Nearly 90% of taxpayers claim the standard deduction vs. itemized deductions. As you prepare to file your next tax return, should you do the same?

Standard deduction vs. itemized deductions

Claiming the standard deduction is certainly easier. To itemize, you need to keep track of what you spent during the year on deductible expenses like out-of-pocket medical expenses and charitable donations. You also need to maintain supporting documentation, such as receipts; bank statements; medical bills; acknowledgment letters from charitable organizations; and tax documents reporting the mortgage interest, real estate taxes, and state income taxes you paid during the year. Then you need to determine whether your available itemized deductions exceed the standard deduction for your filing status.

That might sound like a lot of work, but it can pay off if your total itemized deductions are higher than the standard deduction.

For 2023, the standard deduction numbers to beat are:

- Single taxpayers: $13,850

- Married taxpayers filing a joint return: $27,700

- Heads of household: $20,800

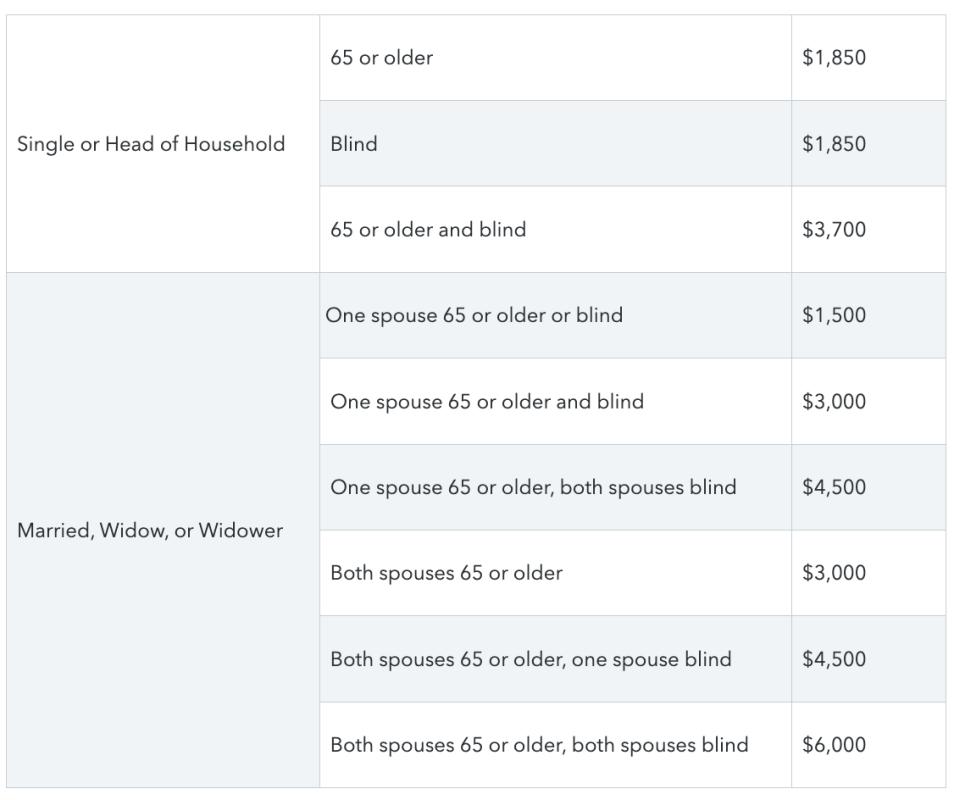

Those are the numbers for most people, but some get even higher standard deductions. If you're 65 or older or blind or both, you may increase your standard deduction by the amount listed below.

Here are a few questions to help you decide whether itemizing deductions might be beneficial for you.

Do you own a home?

For most people who itemize, having a mortgage helps push their itemized deductions higher than the available standard deduction.

In January, your mortgage lender should provide you with Form 1098 (Mortgage Interest Statement). This form might arrive in the mail, be attached to your December or January mortgage bill, or be available to download online.

Form 1098 shows the amount of mortgage interest you paid during the previous year. It may also include any points, mortgage insurance premiums, and real estate taxes you paid through your mortgage servicer.

Tip: Compare your mortgage interest, points, and mortgage insurance premiums to your standard deduction. If the total is larger than your standard deduction, there's a good chance you would benefit from itemizing. All of the rest of your itemized deductions, including state and local taxes, medical expenses, and charitable donations, are just icing on the cake.

Do you pay state and local taxes?

Just about everyone pays some form of state and local taxes. These include:

- Real estate taxes. If you pay your real estate taxes through an escrow account, look at the real estate taxes shown on Form 1098 or the year-end tax summary your lender provided. If your real estate taxes aren't paid through an escrow account, review your property tax bills or canceled checks and add up what you paid.

- State and local income taxes. Add up the state and local income taxes shown on your W-2 and any estimated tax payments you made to your state or local government for this year’s state tax return. Don't forget to add any money you sent with your prior-year state or local tax return.

- Sales tax. If your state and local sales tax is greater than your state and local income taxes, you’ll likely want to deduct sales tax instead. You're allowed to either deduct actual sales tax paid on all of your purchases throughout the year (which requires a lot of record-keeping) or an estimate of what you paid based on your income level and your local sales tax rate. You can estimate your sales tax deduction using the IRS's , or let TurboTax take care of the calculation for you. You can add to this estimate any sales tax you paid on big-ticket items, such as a new vehicle, boat, RV, or major home renovation.

- Personal property taxes. A portion of your annual car registration may be deductible. To qualify, the tax has to be based on the vehicle's value. You can usually find this on your registration or renewal notice.

Add up all of these taxes, but remember the IRS limits your state and local tax deduction to $10,000.

Tip: Add your total state and local taxes (capped at $10,000) to the mortgage interest number you calculated above. If the total is larger than your standard deduction, you'll likely benefit from itemizing.

TurboTax Tip: If you suffered property damage due to a federally declared disaster, you might be able to claim a casualty loss deduction that could tip the scales in favor of itemizing your deductions.

Did you donate to charity?

Add up the money you donated to organizations such as food banks, relief funds, religious organizations, and other nonprofits.

If you donated clothing, furniture, and other household items, you can deduct those as well. To do that, you need to determine their value. One way is to find out what your local thrift store charges for similar items. Or you can use the TurboTax tool called ItsDeductible that does the work for you.

Keep in mind the IRS requires you to keep good records to back up your charitable deductions. For contributions of $250 or more, you need a written acknowledgment from the charity. For donations of less than $250, a canceled check, receipt from the charity, or credit card statement will suffice.

Not all charitable contributions can be deducted on your tax return. Know what you can and can't claim to maximize your potential tax savings.

Tip: For tax years 2020 and 2021 only: Even if you don't itemize deductions, you can still deduct up to $300 of cash charitable contributions on your 2020 tax return (the one you'll file in 2021). You can claim an "above-the-line" deduction on Schedule 1. For tax year 2021, this amount is increased to $600 for married couples filing jointly.

Did you have any out-of-pocket medical expenses?

Although medical expenses are deductible, few taxpayers get to deduct them. That's because you can only deduct costs that exceed 7.5% of your adjusted gross income (AGI).

For example, if your AGI (line 8b of Form 1040) is $50,000 and you have $5,000 of medical expenses, you could only deduct $1,250 of expenses. The first $3,750 of your out-of-pocket costs aren't deductible.

The list of deductible medical expenses is long, but some of the more common ones include:

- Doctor and dentist fees

- Chiropractor fees

- Glasses and contact lenses

- Lab fees

- Long-term care expenses

- Medical supplies

- Prescription medications

You can also deduct the premiums you pay for health, dental, and vision insurance unless you pay for your coverage through your employer using pretax dollars.

Tip: Before you go through all of your doctors' bills and prescription receipts, multiply your AGI by 7.5% and consider whether your out-of-pocket costs are likely to exceed this amount. Taking a minute to do this quick calculation can ensure your time will be well spent.

Do you live in a federally declared disaster area?

If you suffered property damage due to a federally declared disaster, you might be able to claim a casualty loss deduction.

To qualify:

- The federal government must declare the region a disaster area. The Federal Emergency Management Agency (FEMA) maintains a list of disasters searchable by state, year, and type.

- Your loss (after deducting insurance or other reimbursements) has to be more than $100.

- Your total for all casualty losses during the year has to be more than 10% of your AGI.

Tip: If you use TurboTax to prepare your return, you just need to answer some simple questions about your loss. The software will calculate your deduction and fill in all of the right forms for you.

Do you have any miscellaneous itemized deductions?

You may be able to deduct a few miscellaneous expenses, but they're not common.

Before 2018, there were a lot more miscellaneous itemized deductions, but many were eliminated by the Tax Cuts and Jobs Act. Still, a few miscellaneous itemized deductions are available, including:

- Amortizable bond premiums. The amount over face value, or premium, that you pay for certain taxable bonds because they're paying higher-than-current-market interest rates. Premiums on tax-exempt bonds aren't deductible.

- Federal estate tax on income in respect of a decedent. This is an important deduction for taxpayers who inherit money in a 401(k) or IRA account. Such amounts are considered "income in respect of a decedent" because the decedent had a right to the income at the time of death, but the income wasn't included on the person's final tax return. Instead, the beneficiary is taxed on the amounts. You get a deduction, though, if the decedent's estate was large enough to pay federal estate taxes. For example, say you inherit a $50,000 IRA, which, because it was included in your mother's taxable estate, boosted the estate tax bill by $20,500. Although you have to pay tax as you pull money out of the IRA, you also get a deduction for that $20,500. If you pull the full $50,000 out at once, you'll get the full deduction. If you pull it out equally over two years, you can deduct $10,250 each year.

- Casualty and theft losses from income-producing property. You can deduct losses if your income-producing property is damaged or stolen. This includes property held for investment, such as gold, silver, vacant lots, or artwork.

- Some fines and penalties. You can't deduct fines or penalties imposed due to violations of law. However, fines and penalties paid as restitution, remediation, or to come in compliance with a law may be deductible.

- Gambling losses. This write-off comes with restrictions. You can't deduct more than the amount of gambling winnings you report as taxable income.

- Ponzi scheme losses. If you lose money or investments in a Ponzi scheme, the loss is deductible as a theft loss of income-producing property.

- Repayments under claim of right. If you had to repay more than $3,000 that you included in your taxable income in a previous year, you may be able to deduct the amount you repaid.

A final, uncommon category of miscellaneous itemized deductions includes unreimbursed employee expenses for individuals in a qualifying job category. Prior to 2018, these deductions could be made by any employee, but now they're only available to certain performing artists, people in the military reserves, individuals with impairment-related work expenses, and fee-based local or state government officials.

If you have any of the above expenses, it's worth your time to investigate further. Taking the standard deduction might be easier, but if your total itemized deductions are greater than the standard deduction available for your filing status, saving receipts and tallying those expenses can result in a lower tax bill.

With TurboTax Live Full Service, a local expert matched to your unique situation will do your taxes for you start to finish. Or, get unlimited help and advice from tax experts while you do your taxes with TurboTax Live Assisted.

And if you want to file your own taxes, you can still feel confident you'll do them right with TurboTax as we guide you step by step. No matter which way you file, we guarantee 100% accuracy and your maximum refund.