/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

With the advancement of artificial intelligence (AI), Snowflake (SNOW) has emerged as a key player in the cloud-based data warehousing and analytics space. The company offers integrated data storage, processing, and analytics solutions across major cloud platforms such as Amazon (AMZN), Microsoft (MSFT), and Google (GOOGL). Snowflake is gradually becoming the preferred choice for businesses looking to harness the power of their data without requiring extensive infrastructure or complex integrations.

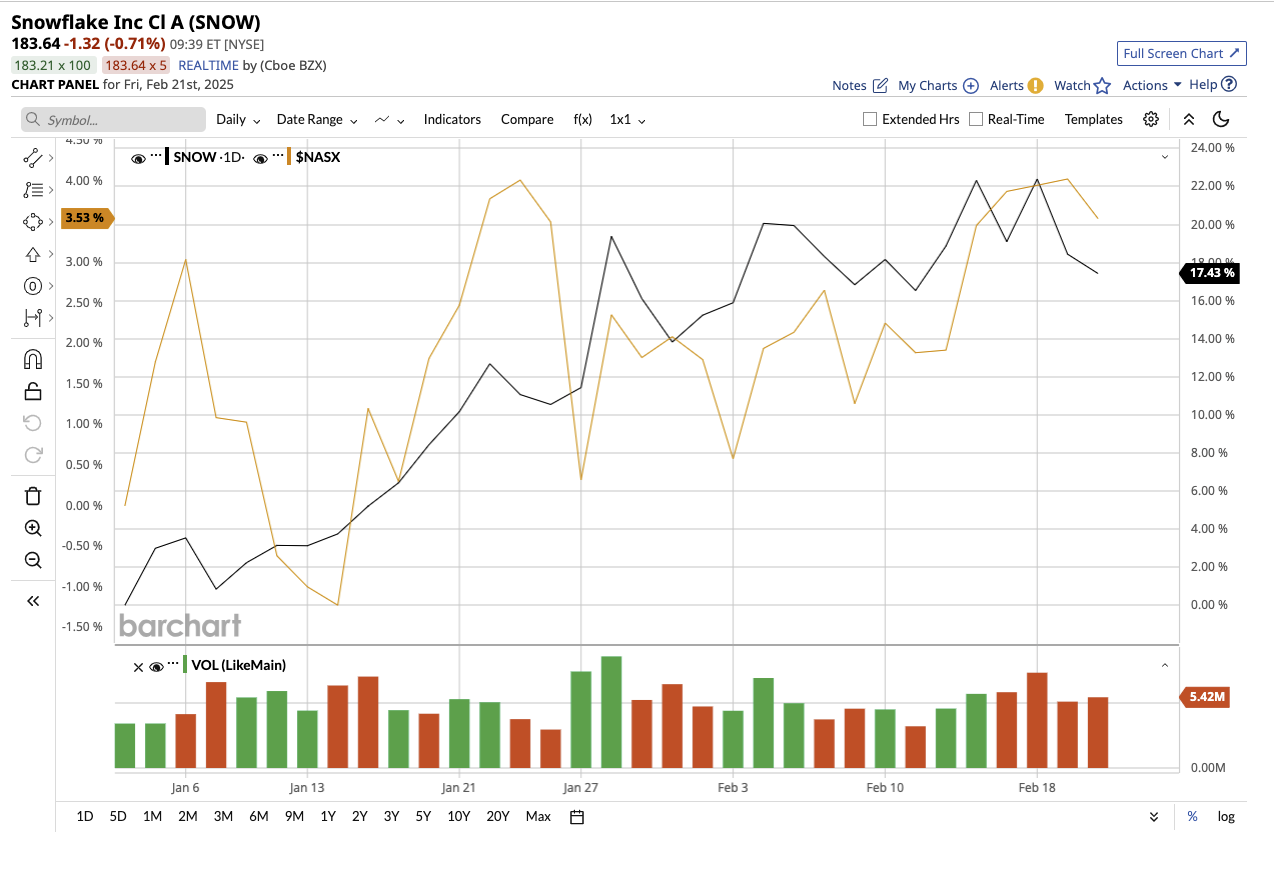

Snowflake is scheduled to report its fourth quarter earnings for its fiscal 2025 on Feb. 26. SNOW stock is up 16.4% year to date, outperforming the tech-heavy Nasdaq Composite Index ($NASX), which is up 3.5%. Let's take a look at its third-quarter earnings and projections for the coming quarter to see if the stock is a good buy now before the earnings are released.

Snowflake’s Financials Are Improving

In the third quarter of its fiscal 2025, Snowflake showcased strong adoption of its AI-driven solutions and cost-effective data management capabilities. The company uses a consumption-based pricing mode that ensures recurring revenue.

CEO Sridhar Ramaswamy stepped into the chief executive role last year. Under his leadership, Snowflake has intensified its focus on integrating AI into its offerings, aiming to provide more robust and intelligent data solutions to its clientele. Snowflake reported product revenue of $900 million for Q3, marking 29% year-over-year growth. Remaining performance obligations (or RPO) that reveal revenue yet to be recognized totaled $5.7 billion, up 55% year-over-year. Additionally, the net revenue retention rate stood at 127%, implying Snowflake is retaining its customers. This performance has prompted Snowflake to raise its annual product revenue guidance for the year, reflecting strong customer demand and trust in its offerings.

While revenue growth has been impressive, profitability remains a question mark for the company. This is not uncommon for growing businesses that invest heavily in R&D, putting pressure on profit margins. Snowflake reported a net loss of $0.98 per share during the quarter. However, the company is taking aggressive steps to streamline operations by forming centralized teams, eliminating redundant management layers, and leveraging AI to increase efficiency while lowering costs. These efforts may help the company turn a profit soon. The company generated an adjusted positive free cash flow of $86.8 million during the quarter.

Snowflake’s AI feature suite, Snowflake Cortex, along with the introduction of Unistore, Snowflake Open Catalog, and the Snowflake Intelligence platform, are propelling the company to the forefront of enterprise AI adoption. Notably, Snowpark assists customers in achieving significant cost savings, with some reporting 50% reductions in data engineering expenses. Moreover, Snowflake's partnership with AWS has resulted in revenue of more than $3.9 billion over the last four quarters. In order to counteract competitive pressures and strengthen its real-time data streaming capabilities, Snowflake is reportedly in talks to acquire RedPanda, a streaming data platform, for around $1.5 billion. This acquisition, if and when it occurs, could strengthen Snowflake’s generative AI roadmap and position it more favorably against competitors. We’ll learn more about this in its most recent quarterly results.

For the fourth quarter, management expects a product revenue increase of 23% to range between $906 million and $911 million. For the full fiscal year, the company expects a 29% increase in product revenue, with adjusted free cash flow accounting for 26% of total revenue. Analysts predict a loss of $0.98 per share on $955.5 million in revenue in the fourth quarter.

For fiscal 2025, analysts predict a 28% increase in total revenue to $3.59 billion, followed by a loss of $0.70 per share. However, analysts expect Snowflake to report a profit of $0.99 in fiscal 2026, led by a 23.2% growth in revenue. Since Snowflake is not profitable yet, we will consider its price-sales ratio for valuation. SNOW stock, which trades at 13.7x forward 2026 sales, remains an appealing cloud computing stock with strong AI potential.

Wall Street’s Opinion Has Changed for SNOW

Recently, TD Cowen analyst Derrick Wood reiterated his “Buy” rating for the stock. With continued demand for its AI offerings and unstructured data solutions, Wood believes Snowflake will outperform future financial targets, setting a $210 price target. Wells Fargo analyst Michael Turrin maintained the same stance.

Interestingly, Snowflake has earned a “Strong Buy” rating on Wall Street, compared to a “Moderate Buy” a month ago. This shift in opinion showcases the trust analysts have in the long-term potential of the company, even though it is not profitable yet.

Out of the 42 analysts covering SNOW stock, 31 have rated it a “Strong Buy,” three suggest a “Moderate Buy,” seven rate it a “Hold,” and one recommends a “Strong Sell.” The stock’s average target price of $194.49 implies 5.15% upside potential from current levels. Further, it has a high target price of $235, which suggests the stock could gain as much as 27% over the next 12 months.

The Bottom Line on SNOW Stock

Snowflake’s platform continues to gain traction in a variety of industries, with high-profile customers such as Warner Bros. Discovery (WBD), Hyatt Hotels (H), and others going all-in on its platform. With iconic brands betting on Snowflake, the company appears poised to lead the data platform industry over the next decade.

However, given that the company is still not profitable, it may be appropriate for investors without a high risk tolerance and a longer investment horizon to wait for the company to reach its full potential.