Insolvency experts say some operators in financial trouble are burying their heads in the sand when it comes to their business finances

Kiwi businesses are being urged to avoid taking a “she’ll be right” attitude, as liquidations in the troubled construction industry are predicted to keep increasing.

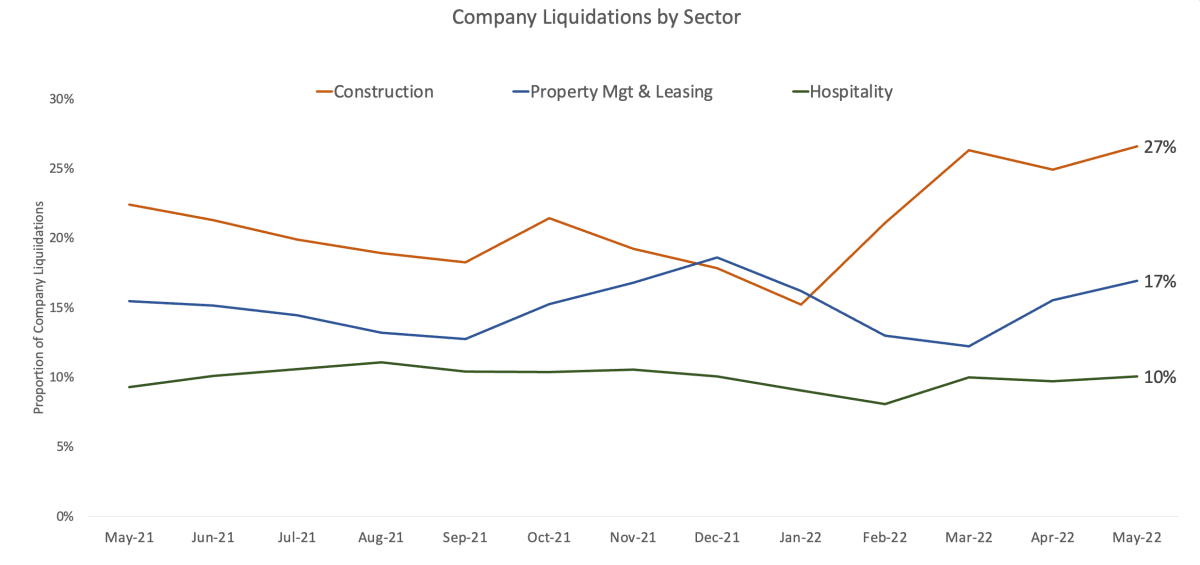

New data from credit rating agency Centrix shows 27 percent of all liquidations in May 2022 were in the building sector. This is up from 18 percent six months ago, as fixed price contracts, supply chain challenges, higher material costs and labour shortages begin to bite, according to the agency.

This is considerably more than in the hospitality sector, which saw only 10 percent of overall liquidations last month.

In the past three months, there have been more than 320 companies placed in liquidation. Of these 86 are in the construction sector.

Of those in the construction industry, 58 percent of the companies are from Auckland, 14 percent from Wellington, 11 percent from Canterbury and 5 percent from the Bay of Plenty.

Wellington-based residential building company Jonesy Construction Ltd is among the businesses who’ve fallen flat.

The business was put into liquidation in May, with Grant Thornton New Zealand’s David Ruscoe and Raymond Cox appointed to the case.

According to the liquidator’s report, Jonesy Construction employed 27 staff and at the date of liquidation there were at least 15 sites under construction.

The company’s director, Benjamin Jones, has advised during 2019 and 2020 that it was undertaking work for a developer who faced financial difficulty.

This resulted in substantial losses to the company, but it was hoped these could be recouped from work in the future.

Company liquidations by industry sector

“The majority of the company’s contracts were … fixed price and were entered into prior to substantial price increases and market fluctuations which caused further losses and time delays that became unsustainable,” the report reads.

The company was placed into liquidation following an assessment of its financial position and “the inability for the director to continue working in the business due to health issues”.

Its statement of financial affairs shows an estimated deficit of $1.5 million. The company’s secured creditors included building supplies companies such as Mitre10 Mega and Carters Building Supplies, with Westpac and ANZ banks.

The company’s records indicated there were unsecured creditors owed a total of $2.1 million.

“At this stage, it is unknown whether there will be any funds available to make payment to unsecured creditors,” according to the report.

The company also owes approximately $411,200 to the Inland Revenue Department.

‘She’ll be right’ attitude not cutting it

Norling Law director Brent Norling says about two-thirds of the liquidations the firm is involved in are within the construction industries, and he expects to see more come through the door.

Norling says the uptick in insolvencies is being exacerbated because the sugar-hit of Government Covid-19 support for businesses who were already struggling before the pandemic is wearing off.

In April 2020, IRD announced it would be writing-off any penalties and interest for businesses unable to pay taxes on time due to the impact of Covid-19.

Norling says many of the companies going into liquidation now were actually insolvent way back in 2019.

This means the impact of the Covid lockdowns of the past couple of years, plus the current building supplies crunch, disrupted supply chain, and labour cost increases might not be felt for a number of years.

“Almost everyone I’ve dealt with has owed money to IRD. They should’ve failed in 2020, but because of a combination of free money and not having consequences for free money, that’s pushed it into this year,” he says.

“That’s a large reason as to why we should expect more insolvencies than in the previous couple of years.”

Norling says it seems as if IRD is picking up enforcement action again, which means business owners who have had their head in the sand will be getting a rude awakening now.

“We were a little bit silent on some of the IRD negotiation work we did.

“Now those inquiries are picking up substantially and we’re dealing with a lot more negotiations for IRD again, which is an indicator that IRD are issuing demands for liquidation proceedings again.”

Inland Revenue customer segment leader Richard Philp says the agency's focus in recent times has been supporting businesses affected by the Covid-19 pandemic through Government support.

Philp says businesses struggling to keep up with tax payments have been encouraged to pay by instalments, and the Government has provided special legislation to allow Inland Revenue to write-off use-of-money interest and late payment penalties for those affected by Covid.

At the end of the 2021 year, the amount of interest and late payment penalties written off under this special legislation was $117m.

In the 2020 year, there were 146,557 instalment arrangements for individuals and businesses set up and in the 2021 year there were 140,000 instalment arrangements covering $3.7b of debt.

While the Government's support initiatives have been the primary focus for IR, Philp says the department is now changing its focus.

"IR is ramping up efforts to engage businesses that have outstanding tax debts and who have not taken any steps to set up a payment arrangement or made contact to discuss their situation," he says.

According to Philp, once the agency understands the circumstances that each business is facing, it can better determine how to address their respective tax debts.

"IR willingly works with business-owners to find answers to their immediate cashflow problems on the basis that our primary responsibility is to “maximise revenue over time,'" he says.

"However, if it is clear that a business is no longer viable, we will take all appropriate action to address current and future debt through the legal processes available to us.

Given the change of tact, there might be some panicking operators out there – Brent Norling is urging businesses to seek help early if they are in trouble.

“A theme in New Zealand is this ‘She’ll be right attitude’. People in these situations do tend to go to ground. They avoid the hard conversations and avoid their creditors.”

Insolvency numbers playing ‘catch up’

PwC business restructuring services leader John Fisk says there have been relatively low insolvencies during the pandemic.

As reported by Newsroom, figures from Government’s Insolvency and Trustee Service (ITS), also known as the Official Assignee’s Office, show ITS-administered liquidations for the more than two years of the Covid-19 pandemic have been at the lowest levels in the almost 20 years for which figures are available.

Fisk, who is also chair of the Restructuring, Insolvency and Turnaround Association of New Zealand, expects more insolvencies will come with an “element of catch-up” at play.

Despite this, and construction traditionally having one of the highest rates of failures in general, he thinks there are ways to help.

“What’s needed is some very pragmatic approaches to dealing with the situation, so the number of insolvencies is minimised.”

This includes good communication between head and sub-contractors, and keeping the cash flowing through the business to reduce the chances of failure.

Fixed price contracts have also caused failures, and companies - such as Jonesy Construction - have learnt this the hard way.

“Moving towards an open book style of contracting in this environment makes a lot of sense, so that the sort of cost escalations and things like that can be shared,” he says.

Fears liquidations would scare away young workforce

Richard Merrifield, a semi-retired builder turned building consultant, agrees open book is the best way to go. He has been in the construction industry since the 1970s and has seen the industry ride the lows and highs of the economy since then.

While he says builders are up against shortages of materials and labour, he thinks operators who have been financially prudent and invested money back into the business to build up capital are coping, while those who are fiscally irresponsible are the ones that should be worried.

If more businesses go bust and staff are made redundant, he is worried young people will be turned off the industry.

“We’re back to square one again. It’s a great industry for young people, but unfortunately the apprentices or young ones are sometimes the first ones laid off and they'll be disillusioned and think, ‘Stuff this, I'll be better off doing something where I've got a secure job’.”

Building Industry Federation of New Zealand chief executive Julien Leys is hearing of more and more liquidations in the sector.

He advises builders not to commit to more projects than they can deal with, and watch their cashflow.

“Where you can talk to your merchant and suppliers, see if you can get a more regular flow of those materials or whether your supplier can do you some kind of deal in the short term,” he says.

“But cash is king, so you've got to protect that cash flow and get paid where you can and not not over commit yourself.”