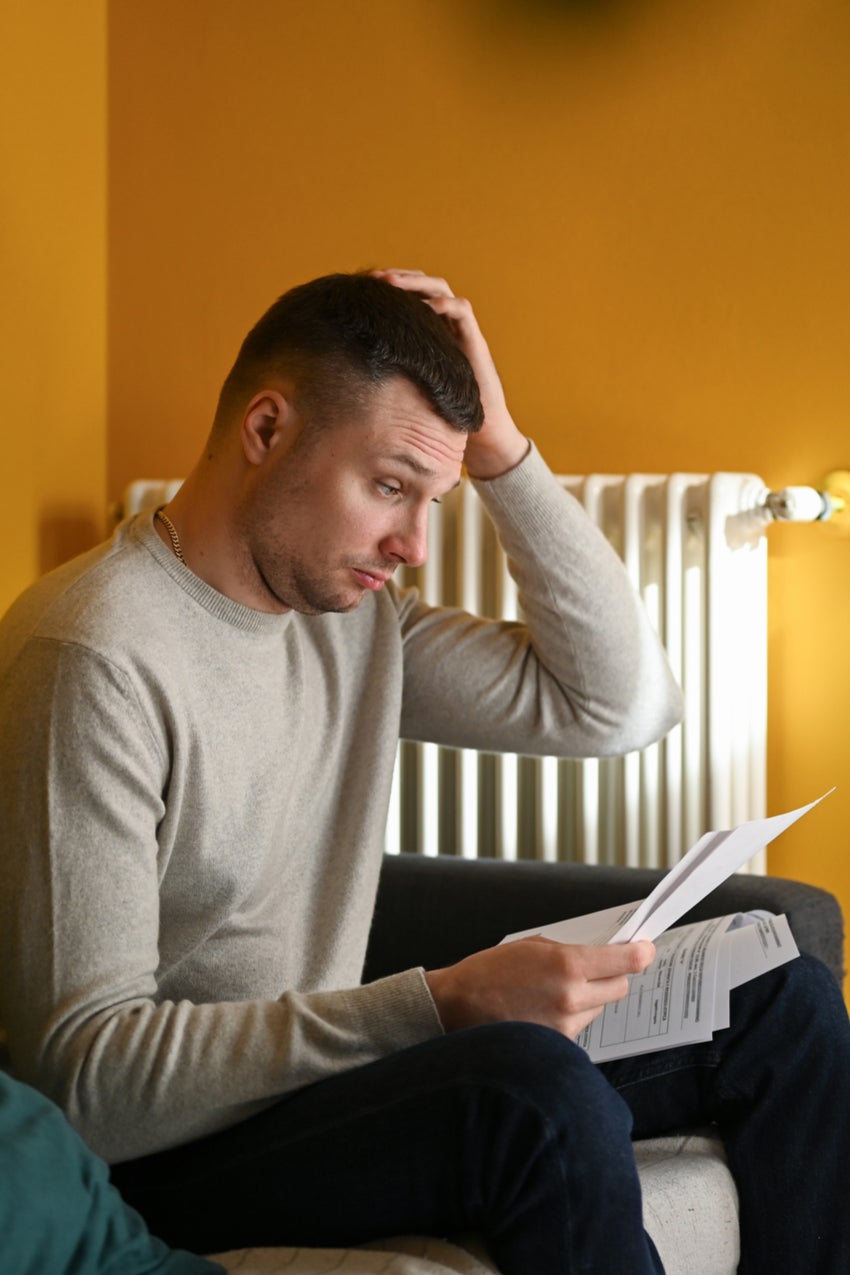

To save money on groceries, Seb Kouyoujmian rummages through the yellow-labelled reduced items in his local supermarket. He won’t buy shoes unless he absolutely needs them. Takeaways are considered a luxury. This might be surprising once you learn Kouyoujmian is an architect on a salary of more than £100,000. But, speaking from the cramped, one-bedroom north London flat he owns, he says that his quality of life doesn’t match what you’d expect given his pay cheque. “I’m earning more than ever before,” the 38-year-old tells me. “But I feel poorer than I ever did.”

It may sound ridiculous to the 96 per cent of the population who typically earn significantly less than £100,000 a year. In fact, the average wage in the UK is around £36,000, according to the Office for National Statistics. For people aged between 18 and 21, it’s closer to £24,000. And it varies according to region, getting worse outside of London.

Yet the fact that the four percenters are feeling the pinch is a symptom of what Dr Mike Savage, a professor of sociology at the London School of Economics and Political Science, calls “intensified” class divisions. In other words, as the wealthy among us struggle to keep up with inflation and the cost of living, their difficulties shed light on just how bad things are getting for the rest of us. Dr Savage helped carry out the largest study on social class in the UK in modern history, and says the situation is urgent.

“The people who are really struggling with cost of living and inflation pressures are those who are badly paid, living in precarious situations, and juggling debts,” he says. “The fear that people on middle and even high incomes are being eroded by inflation and the freezing of tax thresholds is a sign of the sense of insecurity that is felt by large numbers of people.”

The high earners are quite aware of how their laments may be perceived. “It sounds so f***ing privileged,” says Kouyoujmian. “I’m not looking for sympathy, but I’m also trying to be clear that I don’t feel comfortable either.”

Lea Turner, who grew up on a council estate and left school at 16 without an education, agrees. The 39-year-old doesn’t fit the typical trajectory of a six-figure earner, having overcome the challenges of being a single parent on benefits, and going on to build a multi-million-pound company – a digital network of business owners called The HoLT – during the pandemic.

“I feel very lucky to be comfortable because that’s far more than the vast majority of people in the UK can say,” she says. “But it’s not so affordable that I can just rest on my laurels. I still have to maintain this level or the things I have in my life right now will no longer be affordable.”

I have to work 50-70 hours a week, and I still feel like I’m treading water. I know that sounds ridiculous, but I am paranoid about my retirement

Things like her house. After saving for years, and planning her finances, Turner bought a home in Manchester. This year, she found her mortgage increased by £300 a month. “If it goes up much more, I might have to end up selling,” she says.

The cumulative effects of inflation have played a large part, with the Office for National Statistics reporting that a £100,000 salary back in 2000 is worth the equivalent of £53,600 in September 2024 in terms of its value and purchasing power. The Institute for Fiscal Studies also reports that inflation rates for groceries, for example, increased by an average of 26.6 per cent in just over two years, and the effect on households varied according to income. Higher-income households experienced inflation rates 7.7 per cent lower than those in the bottom percentile of households according to income – and what is known as “cheapflation” means that the cheapest products experienced the highest rises. Effectively, the increasing cost of everything means that everyone is getting less bang for their buck.

Although Turner has experienced the precarity of living life on the breadline as a sole earner, she says that earning £100k “definitely doesn’t make you rich”. For example, she expected to be able to afford a new kitchen with ease, but she says that is not the case. “I have to buy and sell clothes on Vinted. I go on an affordable holiday once a year, to the same places I’ve travelled before. It’s not a crazy luxury. I don’t fly first class. We’re not partying on yachts or staying in five-star hotels or anything. I’m not buying designer clothes for me or my son. There are certain things in my life that have upgraded, but not much.”

Kouyoujmian and Turner are known as HENRYs – or “High Earner Not Rich Yet” – a term coined by Shawn Tully in a 2003 article for Fortune magazine, and used to describe people who earn a high wage but don’t have much left after taxes, schooling, housing, family, and saving for retirement. Both Kouyoujmian and Turner understand that they are better off than, for instance, a service worker on a far lower salary. But while a rise in one bill can be a nuisance to the comparatively wealthy, all bills going up at once can leave them in a similar situation to people earning far less.

Kouyoujmian has seen his mortgage and energy bills double and the price of his groceries triple. He says the cumulative cost of all of these increases squeezes resources. As a homeowner and leaseholder, he says he was recently landed with a £21,000 bill, while a cancer scare prompted him to take on private medical care, which has also gone up. Turner, meanwhile, says her outgoings easily add up to £4,000 to £5,000 a month. She pays £1,000 a month in private school fees for her son. This, combined with any emergencies or a holiday, leaves her with little left over.

For Kouyoujmian, an additional worry is his pension. He is currently paying £1,100 into his retirement every month, but because he only started earning six figures three years ago, he has calculated that he will have to pay £3,000 a month to retire at the age of 68 with a £60,000 income. “As an architect, I can’t afford my own service,” he says. “It’s a dream for me to be able to afford someone like me.”

He adds that his quality of life and general work-life balance are poorer than when he earned half his current salary. He’s even taken up a side-hustle making furniture in his spare time. “I have to work 50-70 hours a week, and I still feel like I’m treading water,” he says. “I know that sounds ridiculous, but I am paranoid about my retirement, especially if I look at friends or elderly family members or neighbours and see how they are coping or not coping.”

Investment expert Victoria Harris says that the structure of the tax system means that those earning just above six figures feel the sharpest end of it. She calls it the “60 per cent tax trap”, a name given to the removal of the personal tax allowance for those earning just above £100,000 and below £125,000. A quirk in tax rules means that they can end up paying up to 62 per cent in tax.

In addition to the tax burden, a higher wage can result in “lifestyle creep”, meaning that as you earn more you spend more, opting for more expensive versions of the same things you would have previously bought at a cheaper cost.

Harris, who runs The Curve, a business advising women on their finances, says, “One of our members recently told me, ‘Vic, I fought so hard to break through the £100k ceiling, only to find myself spending even more outside my means than when I was on a lower income.’” She believes that the challenges can be handled with better financial planning. Harris advises “building confidence in salary negotiations”, “creating investment strategies”, and “developing a support network” of other high earners.

However, Dr Savage believes that both tax increases and rising inflation are systemic issues and reflections of the strains on the economy. “Increasingly, in the context of pressures on the welfare state, individuals need to fall back on their private wealth assets to pay for routine medical and other services,” he explains. “Class divisions are being intensified as divides grow between the wealthy and the many who juggle debts.”

If much of their experience sounds familiar, that’s the point. The four per cent aren’t living as luxuriously as we expect, and it should be cause for concern. Because if someone on a big salary can’t afford to remodel their kitchen, or eat out whenever they choose, how can everyone else?