Each week, Next TV writers Daniel Frankel and David Bloom discuss the latest happenings in technology, media and telecom.

DAVID BLOOM: Well, Dan-O, another week of way more news than you’d expect here in August's absolute Dog Days. By the way, I always loved when McGarrett called James MacArthur’s character that on the original Hawaii Five-O. Fun facts about the original: It lasted 12 seasons and a rather insane 281 episodes, and won two Emmys (for music, naturally). It was one of prime time’s most violent shows, routinely perforating the bad guys with bullets back when that was still controversial with critics, Congress and the FCC. But Five-O was also a pioneer, with a far more diverse cast than usual back then, especially of Asian/Pacific Islanders. Harry Endo, Kam Hong, Zulu, Danny Kamekona, Kwan Hi Lim, Tommy Fujiwara and Seth Sakai all booked at least 20 episodes. That more closely mirrored the diverse Honolulu population but wildly contrasted with most Hollywood output back then, when witches, Martians and talking horses were more likely to be featured than people of color,. So, modest progress, then and now. And if you’re a little slow waking up, put that theme song on:

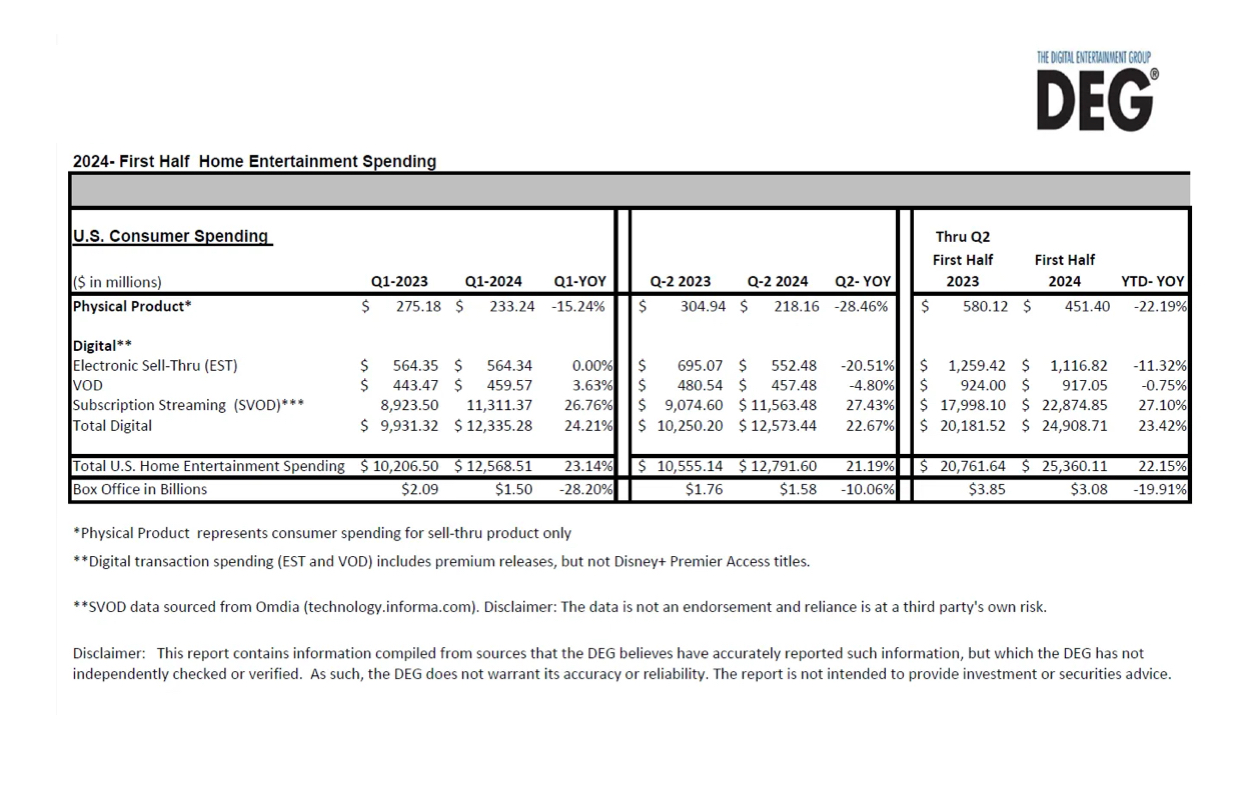

But speaking of throwbacks, the Digital Entertainment Group put out its half-year stats for home entertainment. Streaming is way up, especially FAST and ad-supported premium VOD (think the ad-supported tiers on Hulu, Netflix, Amazon, etc)., which topped $5 billion in ad revenues for the quarter. Overall streaming revenues were up 27 percent, close to $23 billion for the half year. Not bad. Meanwhile, the old-school home-entertainment channels (EST, TVOD) withered like a minor cable network, thanks to the lack of must-watch theatrical releases early in the year. The one growth area there: collectible high-end “Steelbook” and Ultra HD Blu-ray Discs. So, are you still buying the occasional boxed UHD set of, I don’t know, Pirates of the Caribbean? I stopped grabbing any of those before the pandemic, but I’m a little different.

DANIEL FRANKEL: I last played a Blu-ray -- On Any Given Sunday -- in the first month of the pandemic. And that was after digging my player out of mothballs. As for the Digital Entertainment Group, post DVD/Blu-ray, it confounds me a little. Literally 90% of what org deems the measurable U.S. "home entertainment business" is actually subscription video on demand streaming ... as measured by DEG's research partner Omdia. And I might argue that SVOD goes in the "TV" bucket. I'm not sure there's a "home entertainment" anymore. As for Omdia's SVOD data, yes, it always goes up. Because Netflix keeps on growing.

BLOOM: The day's big news, of course, is that a judge granted an injunction freezing the launch of Venu, in response to Fubo’s antitrust case. I recall you thought Fubo had a pretty compelling case. Apparently so does the judge. Normally, an injunction faces a high bar to be granted, especially for a content initiative that hasn’t even launched yet. Two questions: 1.) what’s your take on the judge’s initial decision (a followup hearing is set for next week), and 2.) given this somewhat foreboding initial decision, what are the odds that Venu actually launches at all, ever? That $42.99 monthly price they announced sure doesn’t seem like a winner for consumers, especially minus all those mid-winter NBA games now heading to Peacock. Fubo’s stock spiked on the news (if “skyrocketing” can be defined as moving from $1.30 a share to $1.59 a share), but none of the co-conspirators, er, defendants saw any impact on their suffering share prices. So, what say you?

Also read: Venu Sports Faces Very Real Prospect of Preliminary Injunction

FRANKEL: So this one, part of a joint venture, is hardly all his fault, but count the preliminary injunction slapped on Venu Sports Friday as yet another catastrophe attached to the corporate oversight of one David Zaslav. I mean, you are 100% right, injunctions like these are really hard to get. The judge thought Venu Sports presents an obvious enough threat to market competition and consumer choice that she did what is kind of rare. Zaslav? Iger? Murdoch? They couldn't see around this corner? That's surprising.

I have no idea how Wall Street makes the decisions it does -- I'm not sure Fubo's newfound leverage with its programming distributors makes its future 20% more bright -- but I do suspect it makes the plight of non-sports cable channels even more desperate. The Disney Channel won't be helped when Disney is forced to untether it from ESPN in pay TV licensing negotiations.

BLOOM: I’d put Venu's legal headaches in the “calculated gamble” section of its business plan. They rolled the dice and came up snake eyes, or perhaps more appropriately, craps. Fubo apparently decided this week that it should instead be called Zelig, as in all over the newsreels.

Fubo’s executive chairman the past four years is one Edgar Bronfman Jr., the Seagram’s heir who traded his patrimony to buy Universal, and later headed Warner Music. Now, Bronfman is making a last-minute run at Paramount Global before the “go-shop” provision in David Ellison’s Paramount offer expires in a few days. But, as Rich Greenfield at LightShed Partners suggested in a research note that dropped late Friday, why? David Ellison’s daddy, Larry, is one of the planet’s five richest people. Surely the Ellisons (and partners RedBird Capital, etc) could outbid any offer from the Bronfman group (which includes $500 million from, wait for it, Roku). By Greenfield’s figuring, two points are crucial. One is whether Bronfman can put up enough cash to buy back at least 20% of non-Redstone stock in a proposal that otherwise is less likely to draw shareholder suits. Two is, of course, Shari Redstone, the only voter who matters. If nothing else, this is yet another compelling episode in what was already a five-season corporate soap opera headed straight to series at Apple TV Plus or Max.

FRANKEL: Quickly, my attention got sidetracked by the shiny object which is right-wing sports Twitter. I realize that the No. 1 NFL Draft pick is a legacy fraught with busts, and there are few sure things at the quarterback position.

I want to put this loudly and clearly on the record. I am rooting for the Bears this year. I want them to be good. They deserve it. Ill be sad if Caleb Williams is the bust I think he will be. I want to be wrong.August 17, 2024

But I'm not sure how you look at Caleb Williams and not be pretty sure he'll be a successful NFL quarterback. The improvisation. The accuracy. The poise. It's all there. He showed it to us for three high-level college football seasons with some of the worst offensive lines in the game. He's the closest thing to a sure thing since John Elway, in my quasi-humble opinion. This guy will have a statue in Chicago next to Michael Jordan some day. Just you watch.

Speaking of Max, its losing money again. Parent company Warner Bros. Discovery just took a $9.1 billion write-down on what was, not that long ago, it's most powerful revenue driver, cable networks. Warner stock is at an all-time low. The company is more than $41 billion in debt, and equity analysts are starting to talk about the need for breaking WBD up. Yet, this week, in a co-bylined story, Variety's EIC, Cynthia Littleton, suggested, "The company’s overall financial health is better than it appears, with executives committed to maintaining an investment-grade rating." What oh what could Variety see that we don't? Oh, BTW, took in Alien: Romulus, a respectable minor film franchise event that seemed of little risk to the Alien brand and story canon. The filming location -- and seemingly much of the crew -- was from Budapest. Couldn't have cost a lot for Disney and Fox to come up with this respectable movie for franchise enthusiasts. In fact, Disney could probably take these kind of low-risk plate appearances all day. Kind of reminded me of Gareth Edwards' 2016's Rogue One: A Star Wars Story.

BLOOM: Consider this the Schrödinger’s Cat of the stock market; WBD can be two things at once, both a terrible short-term stock and a long-term potential hit. It’s the process of getting from short to long that’s tricky.

There’s certainly lots to dislike about WBD’s various businesses and their industries, especially for twitchy short-term investors. That’s why shares are down more than two-thirds. It’s a different story for investors willing to hold on for years, not weeks. One key factor: though WBD’s $38 billion in net debt remains huge and ugly, that debt mostly has extremely long repayment schedules (like, into the 2060s). Even better, about 90 percent of the debt is at low fixed rates, safe from interest-rate gyrations. Further, WBD generates lots of cash, which allows the company to pay down some debt early. That cash flow protects WBD's credit rating, if not its regard in the stock market. Though the pared-down Max seems a lot more minimal these days, it’s break-even on costs, no longer a hemorrhaging wound on the balance sheet. That’s what some investors see. Others see a dead cat.