It’s a story as old as time . . . or perhaps as old as gold itself. Mere rumors of the precious metal sent Spanish explorers racing across oceans and pickaxe-wielding prospectors scrambling up California mountains.

Gold is doubtless one of the planet’s most valuable commodities. It’s rare, durable and malleable—not to mention beautiful. Gold has found use in everything from currency to jewelry to electrical conductors inside machinery.

But while many investors turn to gold as a “safety net” in times of market uncertainty, like rising inflation, there are simply more profitable ways to go. Let’s take a look at gold’s history and its role as a “peg” to paper currencies, then examine gold’s performance against consumer prices, debunking the myth of gold as an inflation hedge along the way.

We’ll also stack gold’s performance against the broader stock market over the past 40 years to see just how much luster gold has lost. Finally, we’ll discuss a few better ways to inflation-proof your portfolio—they couldn’t be easier.

A Brief History of the Gold Standard

Simply put, people have been obsessed with gold for millennia. Ancient Romans saw the value in minting gold coins, and because gold was fungible, or easy to trade, they began using it as currency. Egyptians cast intricate sculptures made entirely of gold to honor and remember their pharaohs. In India, where men would inherit the family land and cattle, women would enter a marriage covered in gold jewelry—bangles, pendants, hair accessories and rings—so that they too could own a share of wealth.

For a long time, world currencies, including the U.S. dollar, were pegged to the gold standard, which meant that you could actually go to a bank and exchange paper money for a fixed amount of gold. But World War I caused many nations to temporarily suspend the practice so that they could print more money to fund their militaries, which unfortunately resulted in hyperinflation.

While the Roaring Twenties were a boom time for the American economy, European countries that had borrowed from the U.S. had trouble paying off their debts, causing demand for exports to decline and GDP growth to slow. After the Stock Market Crash of 1929, banks failed, businesses declared bankruptcy, and millions lost their jobs—as well as their savings—resulting in the greatest recession the world has ever known: the Great Depression.

The phrase “once bitten, twice shy” defined sentiment in the 1930s. Fearful of additional bank runs, people began hoarding gold—although stockpiling bullion under one’s mattress would be of little help to the fragile U.S. economy.

Due to the fact that the U.S. dollar was pegged to the gold standard, the Federal Reserve had few tools at its disposal to inject liquidity into the financial system and restart its economic engine—in fact, many now believe this actually prolonged the Great Recession by several years.

So, in an effort to increase the monetary supply, President Franklin D. Roosevelt signed the Gold Reserve Act of 1934, which ended private ownership of gold. This act set the price for gold at $20.67 per ounce, and made people trade in their gold coins and bullion for paper money.

As a result, U.S. stockpiles of gold swelled in places like the Federal Reserve Bank of New York and at Fort Knox, which further increased the U.S. monetary reserves. This would help the economy get back on track until World War II.

Near the end of World War II, the Bretton Woods agreement, signed in July 1944, created an international monetary framework for Allied nations: the United States, Canada, Western Europe and Australia. It reinstated the gold standard yet did so in dollar terms: One dollar was worth $35 per troy ounce of fine gold. It also set a fixed exchange rate relative to the U.S. dollar. To countries scarred by war, this was meant to spur international trade and rebuild trust between nations, although in reality it gave more power to larger central banks who influenced pricing.

The U.S. remained on the gold standard until 1971, when President Richard Nixon ended its convertibility for good. Nixon wanted to increase the monetary supply in order to combat rising inflation.

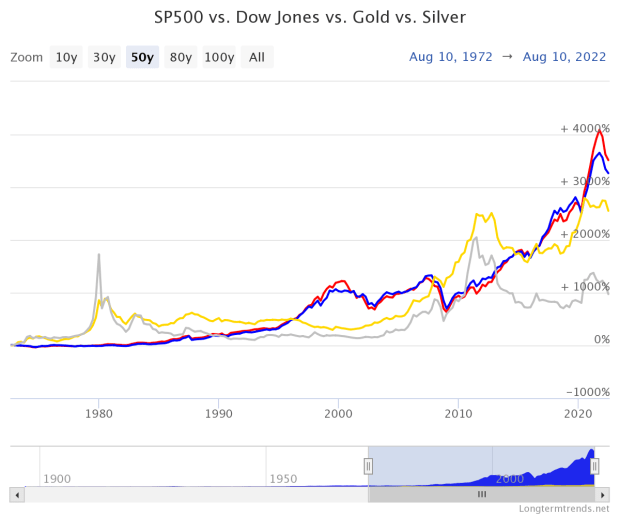

In the years that followed, the value of gold increased by an annualized average of 8.2%, which is impressive until you consider the fact that the S&P 500 actually rose more over the same period. Its annualized average was 11.2%.

Robert R. Johnson, known as an authority on Fed monetary policy, breaks this down even further in his book, Invest with the Fed. In times of rising interest rates, it’s stocks, not gold that do best. "From 1972 through 2013, common stocks returned 14.68 percent in falling rate environments while gold futures returned 7.85 percent.”

Even when interest rates are high, gold underperforms. “In rising rate environments, stocks returned 8.47 percent while gold only returned 4.86 percent.” Johnson continues, “When rates were flat, stocks provided a gain of 10.61 percent and gold returned 8.61 percent.”

So, why buy gold when stock index funds outperform? Clearly, there are plenty of things that glitter more than gold.

Is There Any Upside to Owning Gold?

Still, investors flock to gold during periods of market uncertainty—the Financial Crisis of 2007–2008 and the outset of the COVID-19 pandemic proved that. And it’s true that owning gold can add diversification to your portfolio because, well, there’s nothing else quite like it. Gold is not stocks or equities; it’s not bonds. Gold has its own unique intrinsic value. It will always be valuable, so in that effect, it can act like a safety net.

But the price of gold is volatile: It fluctuates in terms of supply and demand. According to the CBOE Gold ETF Volatility Index, which measures the expected 30-day volatility of returns on the SPDR Gold Shares ETF (GLD), gold’s surges in 2008 and 2020 both ebbed quickly.

Chicago Board Options Exchange, CBOE Gold ETF Volatility Index [GVZCLS], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/GVZCLS, August 9, 2022.

What Are the Downsides of Owning Gold?

There are a few other factors that should give investors pause before they buy gold:

Gold Doesn’t Offer a Dividend

Long-term investors often put their money in well-established companies with a consistent track record of growth and earnings—like blue-chip stocks. Because blue-chip companies are profitable and have been for a long time, many reward shareholders with dividends. These are periodic payments that companies send to their investors based on their profits.

Investors look forward to these regular income payments, especially during bear markets. Gold doesn’t offer a dividend; not even gold ETFs offer dividends. In fact, it actually costs money to own gold when you consider that you need to store it somewhere, which brings us to our next point.

Just Where Do You Keep Your Gold?

Under your bed is always an option, but most investors choose to keep their bullion in a safe deposit box or with a gold storage firm, and fees for boxes just a few feet wide begin at around $50 per year, not including insurance. As a metal and a material, gold is illiquid—unlike bonds, which can be easily converted to cash. In order to sell your gold, you must bring it to a dealer, who will need to verify that the gold is real and will also charge you a premium above the spot price, which reduces your profit.

Gold Has Tax Implications

In addition, Gold is considered by the IRS to be a “collectible,” and so when you sell it, you must pay at the capital gains tax rate of 28%. You cannot own bullion in a Roth or traditional IRA, either. Even gold ETFs are taxed as collectibles—so pay attention.

Finally, let’s examine just how good gold is at fighting inflation . . .

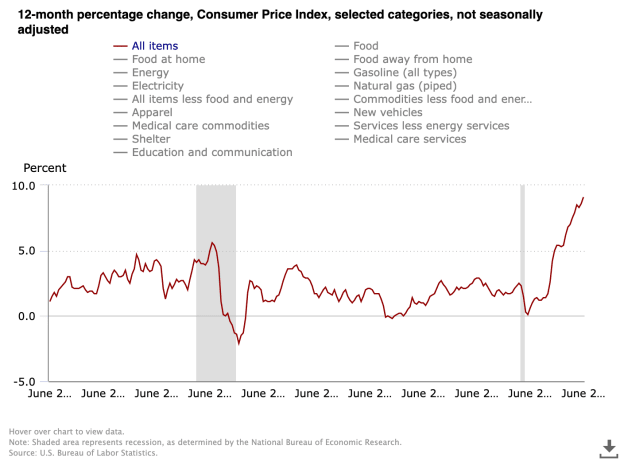

Gold Doesn’t Rise With Consumer Prices

Everyone knows that inflation is a period of rising prices. So, when prices rise, gold’s value should also appreciate, right? The conventional wisdom may say so, but history has proven otherwise, simply because the price of gold has not kept pace with consumer prices.

U.S. Bureau of Labor Statistics.

For example, the consumer price index soared 9.1% in the 12 months through June, 2022, while gold slid 6.3% over the same period.

This could be due to the fact that interest rates were rising, and the Fed used interest rate increases to quell inflation. The price of gold historically has fallen in periods of rising interest rates—not risen.

So, if gold’s not the inflation-fighting hedge we thought it was, what is?

A Few Better Inflation Fighters for Your Portfolio

- Dividend-Paying Stocks: Generally, when inflation’s heating up, the economy is cooling off. Investors turn to value-based investment strategies, including dividend stocks, as a way to shore up their portfolios against volatility while at the same time enjoying steady income payments. Utilities and healthcare are typically value sectors that can withstand market corrections and usually sport a dividend.

- U.S. Treasuries: U.S. Treasuries can also be a better bet. Like dividend-paying stocks, government bonds offer regular interest payments to investors. Plus, they carry the AAA credit rating backed by the “full faith and security” of the U.S. government, which means their risk of default is virtually zero. Both TIPS and I bonds are indexed to inflation, which means their composite yield grows during periods of high inflation.