Designer Brands (NYSE:DBI) is gearing up to announce its quarterly earnings on Tuesday, 2024-12-10. Here's a quick overview of what investors should know before the release.

Analysts are estimating that Designer Brands will report an earnings per share (EPS) of $0.35.

Anticipation surrounds Designer Brands's announcement, with investors hoping to hear about both surpassing estimates and receiving positive guidance for the next quarter.

New investors should understand that while earnings performance is important, market reactions are often driven by guidance.

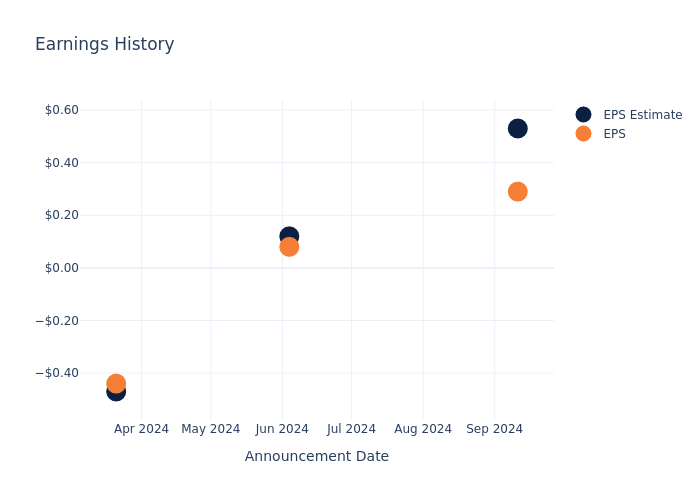

Earnings Track Record

During the last quarter, the company reported an EPS missed by $0.24, leading to a 1.17% increase in the share price on the subsequent day.

Here's a look at Designer Brands's past performance and the resulting price change:

| Quarter | Q2 2024 | Q1 2024 | Q4 2023 | Q3 2023 |

|---|---|---|---|---|

| EPS Estimate | 0.53 | 0.12 | -0.47 | 0.48 |

| EPS Actual | 0.29 | 0.08 | -0.44 | 0.24 |

| Price Change % | 1.0% | -3.0% | 3.0% | -1.0% |

Stock Performance

Shares of Designer Brands were trading at $5.82 as of December 06. Over the last 52-week period, shares are down 30.88%. Given that these returns are generally negative, long-term shareholders are likely unhappy going into this earnings release.

Analyst Insights on Designer Brands

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Designer Brands.

With 4 analyst ratings, Designer Brands has a consensus rating of Neutral. The average one-year price target is $6.88, indicating a potential 18.21% upside.

Peer Ratings Comparison

In this comparison, we explore the analyst ratings and average 1-year price targets of J.Jill, a.k.a. Brands Holding and Citi Trends, three prominent industry players, offering insights into their relative performance expectations and market positioning.

- The consensus among analysts is an Neutral trajectory for J.Jill, with an average 1-year price target of $31.0, indicating a potential 432.65% upside.

- a.k.a. Brands Holding received a Buy consensus from analysts, with an average 1-year price target of $27.5, implying a potential 372.51% upside.

- As per analysts' assessments, Citi Trends is favoring an Buy trajectory, with an average 1-year price target of $24.0, suggesting a potential 312.37% upside.

Peer Metrics Summary

Within the peer analysis summary, vital metrics for J.Jill, a.k.a. Brands Holding and Citi Trends are presented, shedding light on their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Designer Brands | Neutral | -2.56% | $252.91M | 3.87% |

| J.Jill | Neutral | -0.89% | $109.39M | 11.42% |

| a.k.a. Brands Holding | Buy | 6.44% | $86.92M | -3.98% |

| Citi Trends | Buy | 1.42% | $54.93M | -5.36% |

Key Takeaway:

Designer Brands is positioned in the middle among its peers for revenue growth. It ranks at the top for gross profit and return on equity.

Discovering Designer Brands: A Closer Look

Designer Brands Inc is a designer, producer, and retailer of footwear and accessories. The company operates in three reportable segments: the U.S. Retail segment, the Canada Retail segment, and the Brand Portfolio segment. The U.S. Retail segment operates the DSW Designer Shoe Warehouse banner through its direct-to-consumer U.S. stores and e-commerce site. The Canada Retail segment operates The Shoe Company and DSW banners through its direct-to-consumer Canada stores and e-commerce sites. The Brand Portfolio segment earns revenue from the sale of wholesale products to retailers, commissions for serving retailers as the design and buying agent for products under private labels, and the sale of branded products through its direct-to-consumer e-commerce sites.

Unraveling the Financial Story of Designer Brands

Market Capitalization Analysis: The company exhibits a lower market capitalization profile, positioning itself below industry averages. This suggests a smaller scale relative to peers.

Revenue Challenges: Designer Brands's revenue growth over 3 months faced difficulties. As of 31 July, 2024, the company experienced a decline of approximately -2.56%. This indicates a decrease in top-line earnings. As compared to competitors, the company encountered difficulties, with a growth rate lower than the average among peers in the Consumer Discretionary sector.

Net Margin: Designer Brands's net margin lags behind industry averages, suggesting challenges in maintaining strong profitability. With a net margin of 1.79%, the company may face hurdles in effective cost management.

Return on Equity (ROE): Designer Brands's financial strength is reflected in its exceptional ROE, which exceeds industry averages. With a remarkable ROE of 3.87%, the company showcases efficient use of equity capital and strong financial health.

Return on Assets (ROA): Designer Brands's ROA falls below industry averages, indicating challenges in efficiently utilizing assets. With an ROA of 0.65%, the company may face hurdles in generating optimal returns from its assets.

Debt Management: Designer Brands's debt-to-equity ratio stands notably higher than the industry average, reaching 3.59. This indicates a heavier reliance on borrowed funds, raising concerns about financial leverage.

To track all earnings releases for Designer Brands visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.