Since 2005, productivity growth has been lackluster, averaging 1.4% a year, compared to the post-World War II average of 2.2%.

That is a problem. Increasing productivity–economic output per unit of input–maintains U.S. competitiveness and improves our quality of life. It is also essential to meet challenges like inflation, debt loads, entitlements, and the energy transition.

Regaining historical rates of productivity growth could generate a total of $10 trillion for U.S. GDP by 2030, or $15,200 per U.S. household that year.

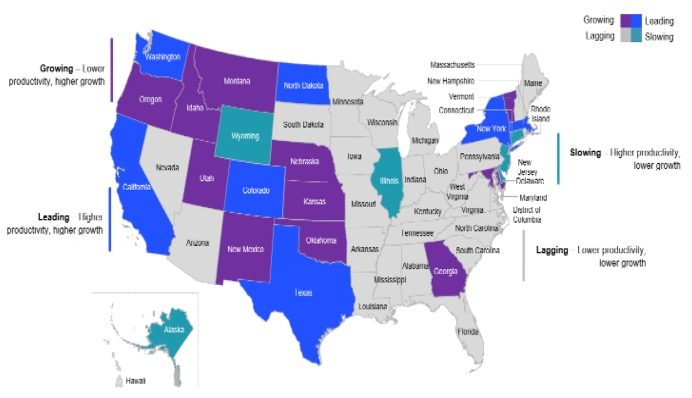

It won’t be easy–but productivity is growing fast in some sectors and geographies. Since 2007, the information sector has grown at 5.5% annually. North Dakota’s economy has grown at nearly 3.5% and Washington’s at 2.3%. We need to improve productivity more broadly.

To get the U.S. economic engine humming, we need to overcome four challenges.

Workforce shortages and skills gaps

There are two separate but linked workforce challenges. One is the lack of workers. U.S. workforce participation rate has fallen to 62.3%, down from 67% in the late 1990s. Only part of this is due to an aging population: More than 5 million Americans are not in the workforce but say they want to work.

The second challenge is that too many current workers do not have the skills they will need to succeed. Skilled talent is essential to productivity growth. In the last 30 years, firms that have invested in people have seen outsized returns. But re-skilling is a process, not a result. As technology changes, so do the skills people need. Hiring for skills rather than credentials–and dropping degree requirements as some states have done–could expand the qualified pool.

Digitization without a productivity dividend

When it works, the link between digitization and productivity is profound: From 1989 to 2019, there was a strong correlation between sectors’ productivity growth and their level of digitization.

Information, finance, and wholesale trade, for example, have all seen rapid productivity growth since 2005, and all are highly digitized. It goes in the other direction, too: the construction industry is the second-least digitalized sector, and has seen next to no productivity growth for a generation. Digitization also helps individual firms grow more productive. In manufacturing, for example, leading firms are more than five times as productive as the laggards.

However, many firms that have invested in digitization are not seeing the benefits. Our research from 2022 showed that most organizations achieved less than a third of the impact they expected from digital investments. Too often, they fail to make the complementary changes across strategy, processes, and training needed to extract full value from digitization.

Leaders distinguish themselves by setting bold business goals enabled by technology. They redesign operational processes rather than augment existing ways of doing business. And perhaps most importantly, they don’t forget the human element: They support individuals and teams to work together effectively in these new models.

Underinvestment in intangibles

Technology by itself is just boxes and bytes: developing it and then putting it to work requires investments in research, intellectual property, and skilled people.

Such expenditure creates a productivity “J-curve” in which the initial benefits may be small (or even negative) but long-term value is substantial. But not all firms invest in the first place. Our research has found that productivity-leading firms invest more than twice as much in intangibles.

Government has a role to play, too, by clarifying and simplifying regulations, and easing constraints on new investments.

Geographic haves and have nots

“The future is already here–it’s just not evenly distributed,” noted William Gibson. And that is true for U.S. productivity. Some states have performed well above average over the last generation. But too many others have below-average productivity and are slipping.

Within states, too, some cities and regions have fallen behind. Such areas often see more than their share of social ills such as lower life expectancy. Even cities with high productivity, such as San Francisco, have not succeeded in distributing gains evenly. Broadly improving productivity is a social as well as an economic issue.

Restoring U.S. productivity growth to its historical rate is not impossible. We’ve done it before. From 1980 to 95, productivity growth was at 1.7%, then accelerated to 3% for the next decade.

Revving up U.S. productivity should be seen a national imperative. We need it to address workforce shortages, manage the energy transition, raise incomes, improve competitiveness–and enhance the lives of all Americans.

Asutosh Padhi is a senior partner in McKinsey & Company’s Chicago office and managing partner for North America. Olivia White is a director of the McKinsey Global Institute in San Francisco.

The opinions expressed in Fortune.com commentary pieces are solely the views of their authors and do not necessarily reflect the opinions and beliefs of Fortune.

More must-read commentary published by Fortune:

- A soft landing is playing out—but optimism needs to be for the right reasons

- Overconfident tech CEOs have overpaid for ‘box tickers’ and ‘taskmasters.’ Here’s why the real ‘creators’ will survive the mass layoffs

- The U.S. has thwarted Putin’s energy blackmail. Europe says ‘Tanks a lot!’

- I am a DoorDash driver who’s been elected to the Colorado State House. Food delivery companies are gamifying your tips and making it harder for drivers to earn a living wage. Here’s what you can do about it