Foot Locker (NYSE:FL) will release its quarterly earnings report on Wednesday, 2024-12-04. Here's a brief overview for investors ahead of the announcement.

Analysts anticipate Foot Locker to report an earnings per share (EPS) of $0.42.

The announcement from Foot Locker is eagerly anticipated, with investors seeking news of surpassing estimates and favorable guidance for the next quarter.

It's worth noting for new investors that guidance can be a key determinant of stock price movements.

Historical Earnings Performance

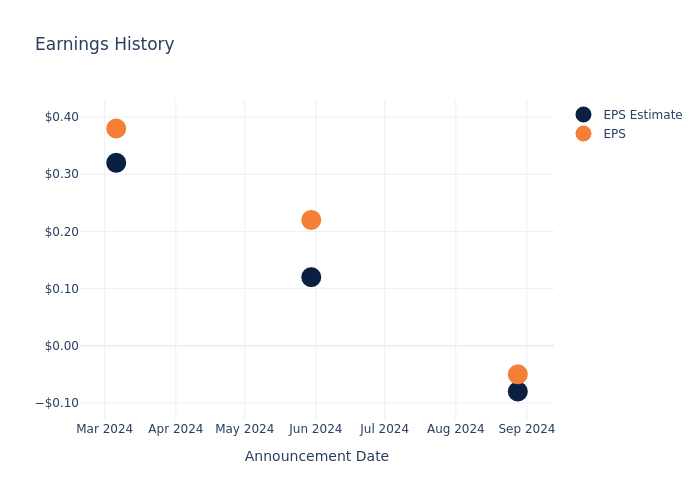

The company's EPS beat by $0.03 in the last quarter, leading to a 6.28% increase in the share price on the following day.

Here's a look at Foot Locker's past performance and the resulting price change:

| Quarter | Q2 2024 | Q1 2024 | Q4 2023 | Q3 2023 |

|---|---|---|---|---|

| EPS Estimate | -0.08 | 0.12 | 0.32 | 0.25 |

| EPS Actual | -0.05 | 0.22 | 0.38 | 0.30 |

| Price Change % | 6.0% | 7.000000000000001% | 0.0% | -3.0% |

Performance of Foot Locker Shares

Shares of Foot Locker were trading at $25.14 as of December 02. Over the last 52-week period, shares are down 11.04%. Given that these returns are generally negative, long-term shareholders are likely bearish going into this earnings release.

Analyst Observations about Foot Locker

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on Foot Locker.

The consensus rating for Foot Locker is Neutral, derived from 6 analyst ratings. An average one-year price target of $27.0 implies a potential 7.4% upside.

Comparing Ratings with Competitors

In this analysis, we delve into the analyst ratings and average 1-year price targets of Revolve Gr, Buckle and Victoria's Secret, three key industry players, offering insights into their relative performance expectations and market positioning.

- Revolve Gr is maintaining an Neutral status according to analysts, with an average 1-year price target of $29.75, indicating a potential 18.34% upside.

- The consensus outlook from analysts is an Neutral trajectory for Buckle, with an average 1-year price target of $46.0, indicating a potential 82.98% upside.

- The consensus among analysts is an Neutral trajectory for Victoria's Secret, with an average 1-year price target of $33.0, indicating a potential 31.26% upside.

Overview of Peer Analysis

The peer analysis summary provides a snapshot of key metrics for Revolve Gr, Buckle and Victoria's Secret, illuminating their respective standings within the industry. These metrics offer valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Foot Locker | Neutral | 1.93% | $527M | -0.41% |

| Revolve Gr | Neutral | 9.92% | $144.87M | 2.66% |

| Buckle | Neutral | 3.98% | $132.53M | 9.33% |

| Victoria's Secret | Neutral | -0.70% | $501M | 7.15% |

Key Takeaway:

Foot Locker ranks at the bottom for Revenue Growth among its peers. It is in the middle for Gross Profit. For Return on Equity, Foot Locker is at the bottom compared to its peers.

All You Need to Know About Foot Locker

Foot Locker Inc operates thousands of retail stores throughout the United States, Canada, Europe, Asia, Australia, and New Zealand. It also has a presence in the Middle East. The company mainly sells athletically inspired shoes and apparel. Foot Locker's merchandise comes from only a few suppliers, with Nike providing the majority. Its portfolio of brands, includes Foot Locker, Kids Foot Locker, Champs Sports, WSS, and atmos. The company has omnichannel capabilities to bridge the digital world and physical stores, including order-in-store, buy online and pickup-in-store, and buy online and ship-from-store, as well as e-commerce. It has three operating segments, North America, EMEA, and Asia Pacific.

Foot Locker: A Financial Overview

Market Capitalization Perspectives: The company's market capitalization falls below industry averages, signaling a relatively smaller size compared to peers. This positioning may be influenced by factors such as perceived growth potential or operational scale.

Positive Revenue Trend: Examining Foot Locker's financials over 3 months reveals a positive narrative. The company achieved a noteworthy revenue growth rate of 1.93% as of 31 July, 2024, showcasing a substantial increase in top-line earnings. As compared to competitors, the company encountered difficulties, with a growth rate lower than the average among peers in the Consumer Discretionary sector.

Net Margin: The company's net margin is below industry benchmarks, signaling potential difficulties in achieving strong profitability. With a net margin of -0.63%, the company may need to address challenges in effective cost control.

Return on Equity (ROE): Foot Locker's ROE falls below industry averages, indicating challenges in efficiently using equity capital. With an ROE of -0.41%, the company may face hurdles in generating optimal returns for shareholders.

Return on Assets (ROA): Foot Locker's ROA is below industry averages, indicating potential challenges in efficiently utilizing assets. With an ROA of -0.17%, the company may face hurdles in achieving optimal financial returns.

Debt Management: Foot Locker's debt-to-equity ratio is below industry norms, indicating a sound financial structure with a ratio of 1.01.

To track all earnings releases for Foot Locker visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.