Dividend Aristocrats are an attractive group of stocks for dividend growth investors because of their blue chip quality and proven track record. The stocks pay reliable dividends and grow their distributions annually, helping to compound returns and offset inflation. The best time to buy these stocks is when they are down to maximize cost and yield.

The stocks on this list include Dividend Aristocrats that have been under pressure for years and are trading at the low ends of their respective P/E multiple ranges and at the high end of their dividend yield ranges. The takeaway is that these stocks yield more than 3% each, come with an average yield near 3.7%, and won’t stay down forever. There is reason to believe the rebound could begin in 2025 and rallies sustained over the next two to three years. Falling interest rates, easing regulations, and tax reductions are expected to provide catalysts and tailwinds for the economy and stocks.

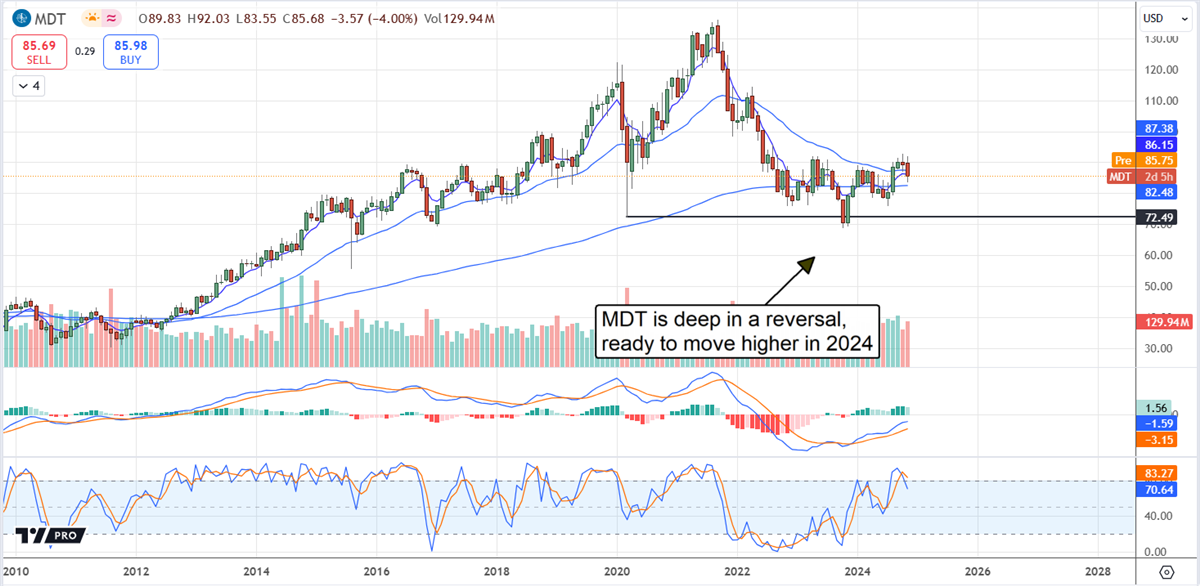

Medtronic Wallows Near Long-Term Lows: Reversal Is in Sight

Medtronic (NYSE: MDT) stock has wallowed near long-term lows for years, but the bottom is in sight. The market is forming a head-and-shoulders pattern, likely leading to a complete reversal and uptrend in 2025. The company’s problem isn’t growth so much as profits. The company sustains mid-single-digit growth but has had margin issues, which management is correcting. The forecast is for earnings to grow nearly 7.5% in 2025 after a tepid low-single-digit performance in 2025 and for the dividend to be sustained. Medtronic has increased its dividend for nearly 50 years. Analysts rate it as a Hold and see it rising more than 10% at the consensus estimate. The estimates are rising in 2024 and provide some lift for the market; that trend will likely continue.

PepsiCo Reverts to Trend

PepsiCo's (NASDAQ: PEP) stock price has increased since 2022, when the pantry-hoarding craze peaked and post-pandemic normalization set in. Since then, the company has struggled to invigorate growth, with revenue trending flat in 2024. Although the company faces headwinds, it has invested in long-term growth, including expanding international markets and internal efficiency. The net result is wider margins, with the 2024 operating margin up by a mid-single-digit figure and expected to remain solid. Regarding the value and yield, PepsiCo stock is trading below 20x earnings in late 2024, more than five handles below average and double that amount below the peak while yielding roughly 3.35%.

Genuine Parts Company Hits Bottom: Growth Is Accelerating

Genuine Parts Company (NYSE: GPC) struggled with growth for the last two years as economic headwinds mounted and industrial demand faltered. However, the company was able to sustain growth, and now it is on the rebound. Revenue growth accelerated to 2.5% in FQ3 2024 and is expected to maintain that pace in Q4 and then accelerate again in 2025. The bar for Q4 is set low because nearly 100% of analysts tracked by MarketBeat lowered their targets this quarter; there is potential for a catalyst in the results.

Target’s Struggles With Existential Threat: Lost Relevance in Age of Consumer Consciousness

Target’s (NYSE: TGT) struggles were and continue to be numerous, including losing market share. It lost market share because of the perceived premium to shop there compared to retailers like Walmart (NYSE: WMT), Costco (NASDAQ: COST), and other value-oriented merchants who continue to lead the sector. The critical takeaway is that the company has reverted to growth, sustains a healthy margin, and provides substantial capital return. The outlook is cloudy, but this business will unlikely fade away. The more likely scenario is that it will regain footing. With easing monetary headwinds and policy tailwinds expected in 2025, the rebound could begin by mid-year 2025, if not sooner. The holiday season guidance was very weak and could easily be exceeded.

Archer-Daniels-Midland Retreats to Critical Support

Archer-Daniels-Midland’s (NYSE: ADM) share price imploded in early 2024 as accounting errors surfaced and earnings and guidance were restated. The scandal is ongoing but unlikely to end the company’s operations. With the shares trading at a multi-year low and critical support, the share price is unlikely to fall further. It is a deep value at this level, trading at only 11x earnings, and the dividend is reliable. The dividend is well-covered even with a reduced outlook for earnings, and offers a nearly 3.75% yield. The business outlook is solid and can sustain annual distribution increases, although the pace may slow from the high-single-digit CAGR it has run to a lower single-digit figure.

The article "5 Dividend Aristocrats to Buy Now and Hold Through 2025" first appeared on MarketBeat.