Biotech companies make some of the best growth stocks.

These firms are at the forefront of medical advances such as gene editing, immunotherapy, artificial intelligence (AI)-driven drug discovery, and precision medicine. Breakthroughs in these areas can drive massive revenue growth and open up new market opportunities, resulting in a significant stock price surge. While biotech growth stocks are risky, they also have high reward potential for long-term investors willing to navigate volatility and regulatory hurdles. Here are two such growth stocks that investors may want to consider now.

Growth Stock #1: Arcturus Therapeutics

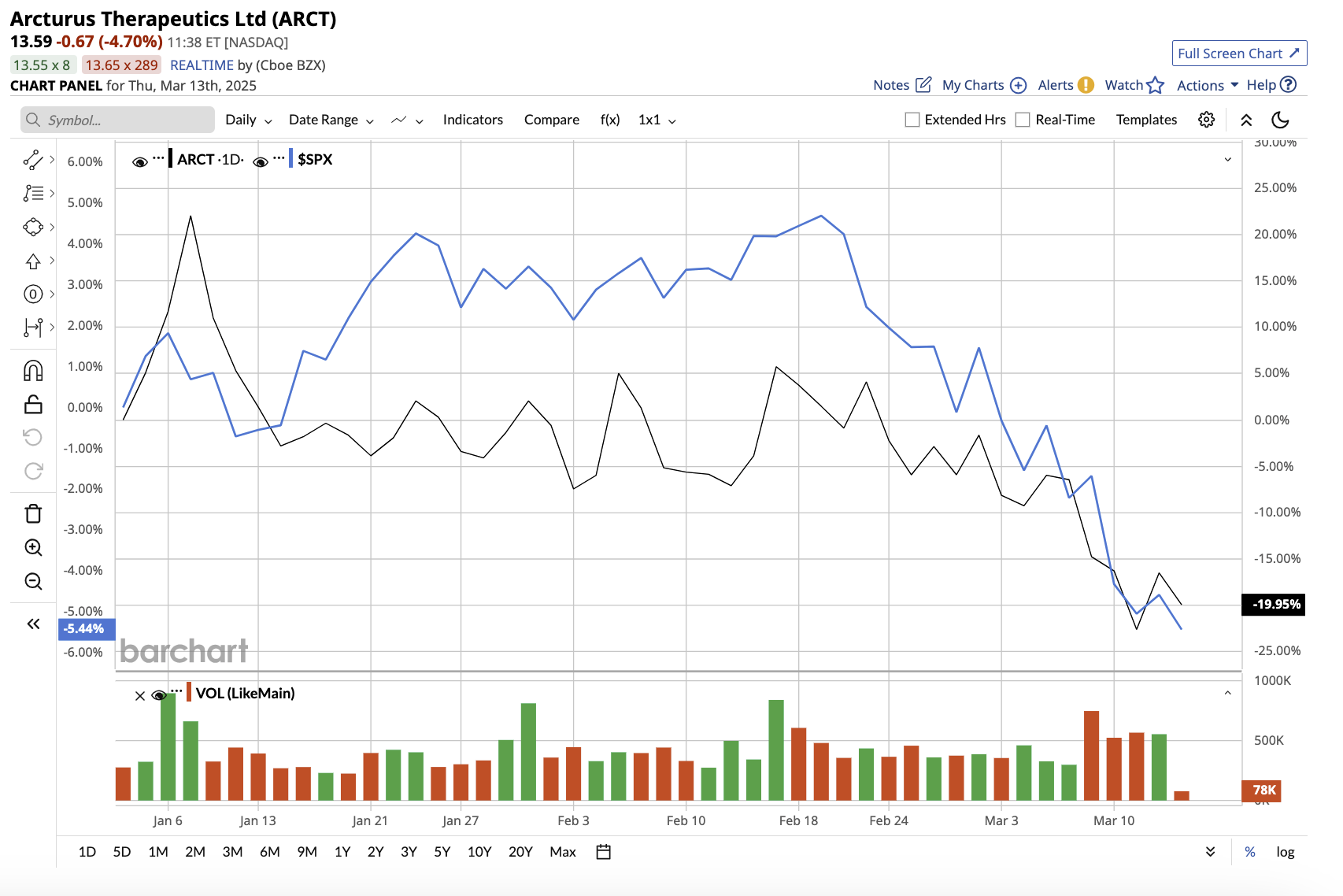

Arcturus Therapeutics (ARCT) is a biotech company that is making significant progress in the development of messenger RNA (mRNA) medicines for infectious diseases, rare liver diseases, and respiratory conditions. Valued at a market cap of $377 million, Arcturus stock has dipped 18% year-to-date, compared to the S&P 500 Index ($SPX) fall of 5.1%.

Arcturus has been actively developing its pipeline. In December 2024, the company began dosing in a Phase 2 study for ARCT-032, an mRNA therapeutic candidate for cystic fibrosis (CF). The company expects interim results from the Phase 2 trial by the end of the second quarter of 2025. Additionally, the company is conducting a Phase 2 trial with ARCT-810, an mRNA therapeutic candidate for ornithine transcarbamylase (OTC) deficiency. Interim results are expected by the end of the second quarter of 2025.

Aside from these two candidates, Arcturus has collaborated with several companies to build a robust and diverse preclinical mRNA therapeutic and vaccine pipeline. In February, the company reached another significant milestone when the European Commission approved KOSTAIVE, making it the world’s first self-amplifying mRNA COVID-19 vaccine. Prior to this, Arcturus’ manufacturing joint venture ARCALIS and Meiji Seika Pharma received approval from the Ministry of Health, Labour, and Welfare (MHLW) in January to expand KOSTAIVE’s commercial manufacturing sites in Japan.

For the time being, the company generates no product revenue, rather relying on licensing, consulting, and other technology transfer fees. Net revenue in the fourth quarter stood at $22.8 million, with total revenue of $152.3 million for fiscal year 2024. At the end of the quarter, Arcturus had a strong cash position of $293.9 million, providing a financial runway through the first quarter of 2027.

Arcturus’ diversified pipeline, which includes both vaccines and therapeutics for rare diseases, provides numerous opportunities for growth. However, as with any biotech stock, it faces the risk of clinical trial failures or regulatory approval delays.

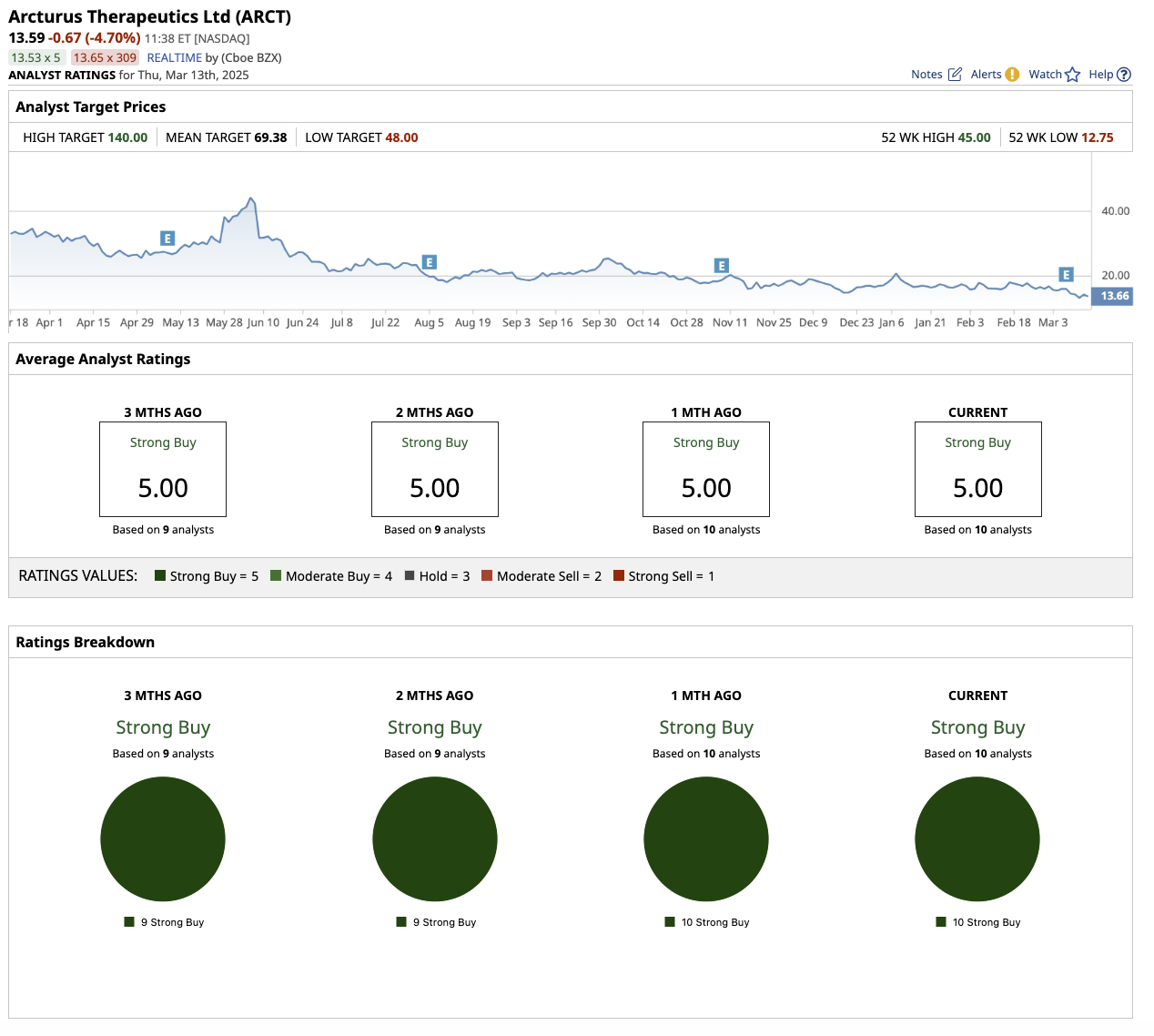

Overall, Wall Street rates Arcturus stock a “Strong Buy.” Out of the 10 analysts covering the stock, all rate it a “Strong Buy.” The average target price of $69.38 suggests the stock can rally as much as 410.5% over current levels. Plus, the high target price of $140 suggests upside potential of 930% over the next 12 months.

Growth Stock #2: Phathom Pharmaceuticals

With a market cap of $293.8 million, Phathom Pharmaceuticals (PHAT) is a commercial-stage biotech company that has gained traction for its focus on developing treatments for gastrointestinal (GI) diseases. Phathom currently has an approved product called VOQUEZNA (vonoprazan) in its lineup. In July 2024, the FDA approved VOQUEZNA 10-mg tablets to treat heartburn in adults with non-erosive gastroesophageal reflux disease (GERD).

In its first full year of launch, it generated net revenues of $55.3 million, including $29.7 million in the fourth quarter of 2024. Since its launch, the company has filled more than 300,000 prescriptions for VOQUEZNA products. Phathom stock is down 45% in the year-to-date. Nonetheless, Wall Street predicts the stock to soar this year.

Aside from GERD, VOQUEZNA is approved for the treatment of erosive esophagitis and, when combined with antibiotics, for the eradication of H. pylori. Net revenue in the fourth quarter stood at $29.7 million, driven primarily by the successful launch and market penetration of VOQUEZNA, VOQUEZNA TRIPLE PAK, and VOQUEZNA DUAL PAK. However, as a commercial-stage company, it will take time to become profitable. Net loss in the fourth quarter stood at $74.5 million, a slight improvement from the $79.6 million loss in Q4 2023.

Phathom is exploring additional therapeutic applications for VOQUEZNA. A Phase 2 study is planned to evaluate VOQUEZNA’s potential for treating Eosinophilic Esophagitis (EoE) in adults and adolescents, with enrollment expected in the first half of 2025. At the end of the fourth quarter, Phathom had $297.3 million in cash and cash equivalents, with an additional $100 million available through a term loan with Hercules. The company believes that the funds will be sufficient to fund operations until it becomes cash flow positive.

The commercial rollout of VOQUEZNA has been met with encouraging market adoption. For the full year 2025, analysts predict revenue growth of 195.3% to $163.1 million, followed by an increase of 115.2% to $351.2 million in 2026.

Overall, Wall Street rates Phathom stock a “Strong Buy.” Out of the eight analysts covering the stock, six rate it a “Strong Buy,” one says it is a “Moderate Buy,” one rates it a “Hold.” The average target price of $21.62 suggests the stock can rally as much as 367% over current levels. Plus, the high target price of $28 suggests upside potential of 504.7% over the next 12 months.

Phathom’s strong financial performance in 2024, combined with strategic product development initiatives, sets it up for future growth. However, given that it is still in the pre-profit stage, investors should conduct extensive research before considering this growth stock.