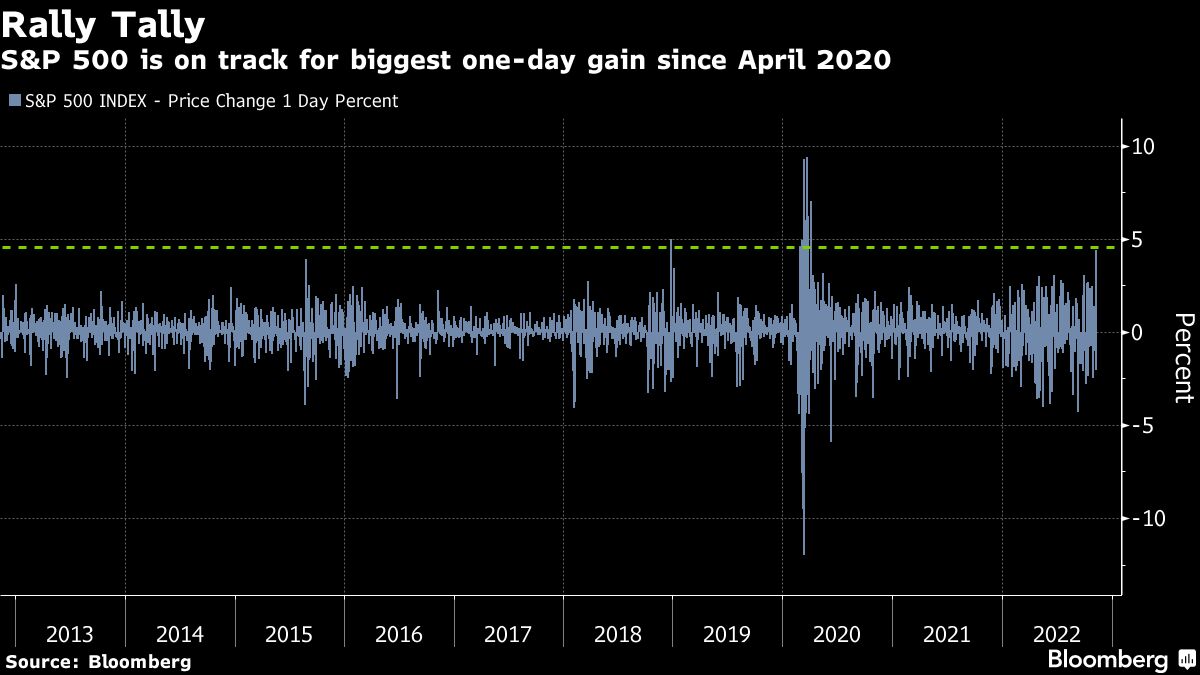

The euphoria that’s sweeping through the stock market Thursday has strong justification in history: whenever inflation has peaked, double-digit gains have followed.

The S&P 500 Index, which has shed 18% in 2022, surged 4.7% on Thursday after the rise in the consumer price index cooled in October by more than forecast, putting the index on track for its best CPI day since December 2008. Meanwhile, the Nasdaq 100 Index soared 6.1%. Both indexes are on pace for their best sessions since April 2020.

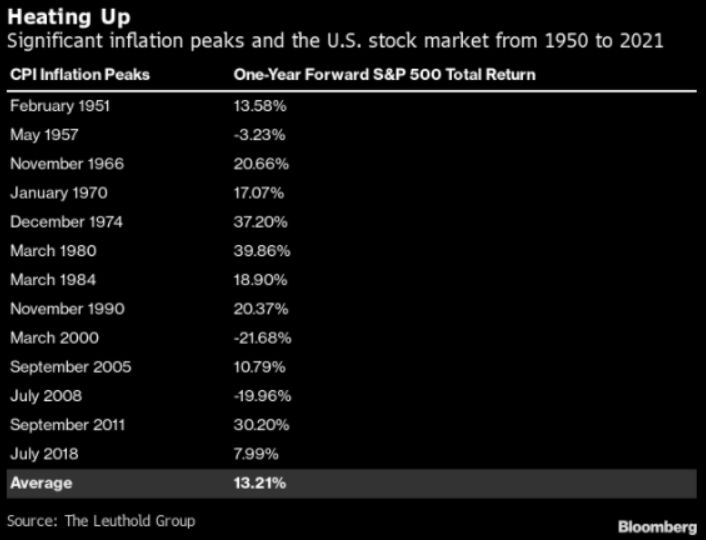

Not surprisingly, US stocks struggle while inflation rises, but not after it peaks. Since 1950, the S&P 500 has posted a total return of 13% on average over the next 12 months following 13 major inflation peaks, according to Jim Paulsen, chief investment strategist at The Leuthold Group. In the 10 instances where the index rose the year following a substantial inflation spike, the total return for the S&P 500 jumped by an average of 22% over the subsequent year, data from Leuthold show.

While nobody knows whether the bear market is nearing its end or if it is due for another leg lower, Paulsen noted that “bad news” has seemingly affected the stock market far less since the summer than in the first half of 2022. That’s come with cyclical sectors and small-cap stocks soundly beating the S&P 500 in recent months, he added.

For US equity markets to see comparable gains, stubbornly high inflation rates must fall at a faster clip, though investors may miss out on those hefty gains if they wait too long since markets tend to begin rallying from bear market lows well before economic data bottoms, according to Jimmy Lee, chief executive of The Wealth Consulting Group.

“Investors really need to be positioned well in advance of the Fed signaling a pause because the stock market will likely be substantially higher from here by the time those words come out of Fed Chair Powell’s mouth,” Lee said.

In post-World War II cycles when consumer price increases topped 5%, the benchmark’s average return six months, one year and two years later was 5%, 12% and 15%, respectively, according to Strategas Research Partners.

Federal Reserve officials have been aggressively raising borrowing costs in an effort to cool inflation running near 40-year highs. The central bank hiked interest rates by 75 basis points for the fourth straight time last week, bringing the target for the benchmark rate to a range of 3.75% to 4%. Fed Chair Jerome Powell told reporters after the decision that recent disappointing data suggest rates will ultimately need to go higher than previously expected, while indicating the central bank could moderate the size of its increases as soon as December.

Philadelphia Fed President Patrick Harker and Dallas Fed President Lorie Logan recently said they expect the central bank to slow the pace of rate hikes in upcoming months as US monetary policy approaches restrictive levels. But Logan noted at a conference hosted by her bank in Houston Thursday that it “should not be taken to represent easier policy.”

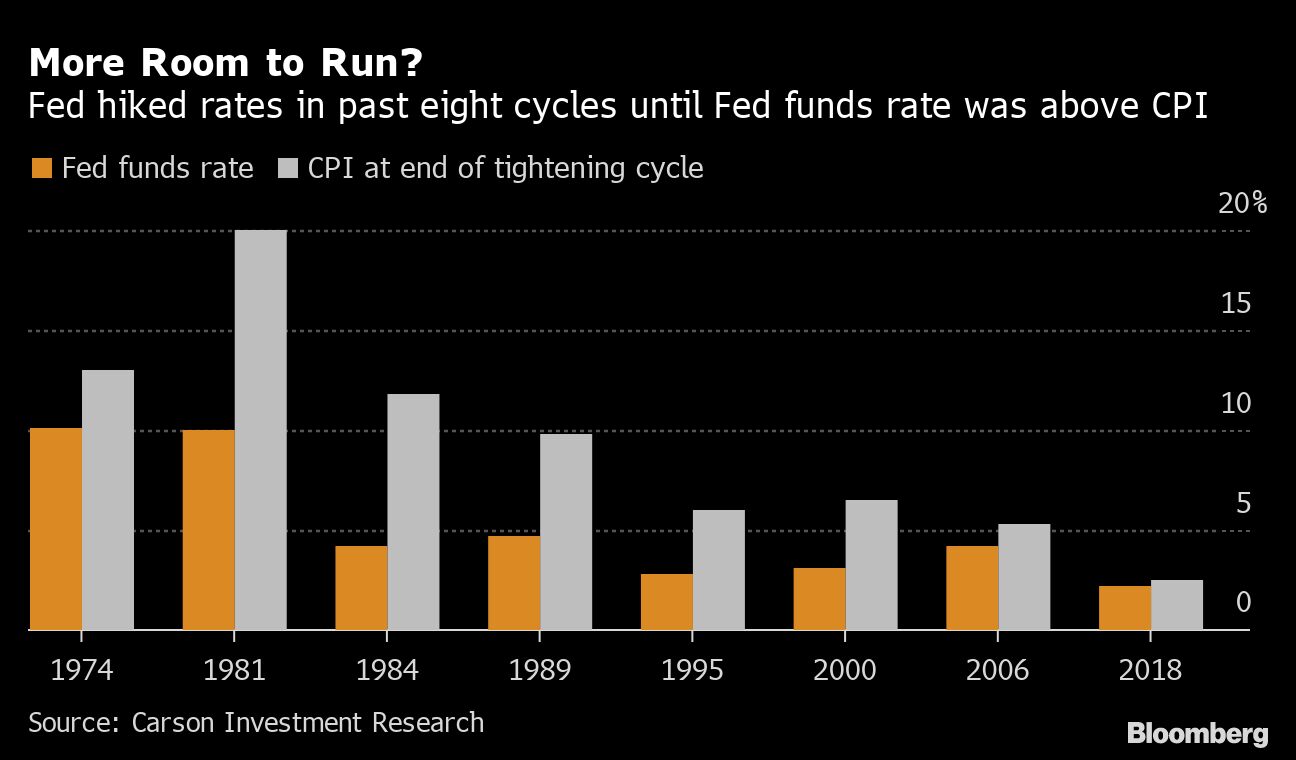

Still, the past eight rate-hiking cycles saw the Fed continue to lift borrowing costs until it was above CPI, according to Carson Investment Research. Market for wagers on the Fed’s policy rate priced in a peak of 4.8% for the first half of 2023, edging down from above 5% last week. That means there still could be more room for the Fed to lift rates to tame stubbornly high prices.

©2022 Bloomberg L.P.